Commodity stocks are neglected, unpopular, and generally overlooked. That is exactly why they are so interesting to contrarian investors.

For the last decade, investors have been focused mainly on high-growth tech stocks. That has had a direct impact on commodities and heavy industry. Why sink billions in mines, refineries, or steel mills when a company employing a few dozen programmers can create a unicorn startup?

At the same time, there’s a quiet case for commodities. They are always needed and never out of fashion. Companies often have very low valuations, and many pay solid dividends.

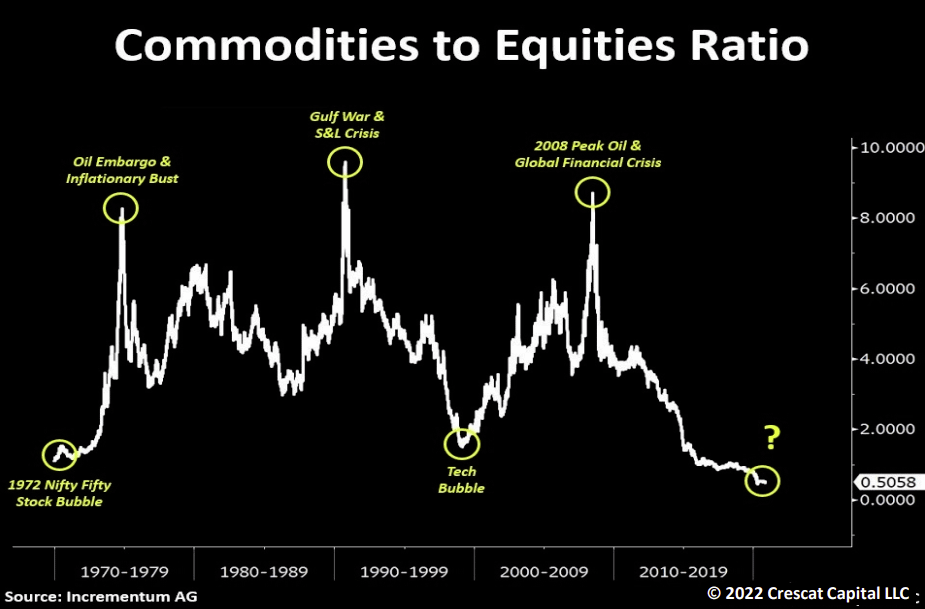

Commodities are currently at a cyclic low relative to equity markets overall.

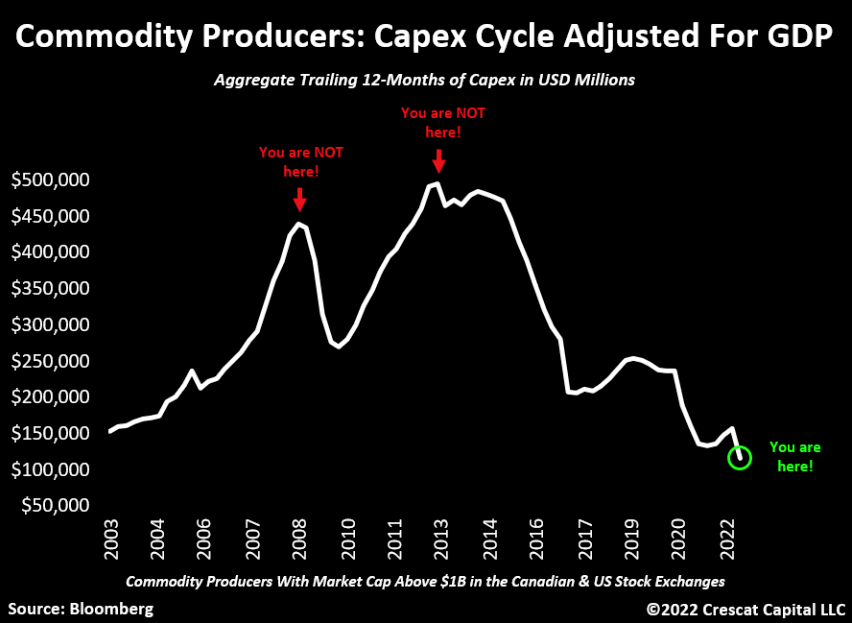

Commodity producers are also at a low point in their investment cycle, suggesting that commodity prices could be set to rise.

If that sounds interesting, take a look at these top commodity stock picks from around the world.

Best Commodities Stocks

Let’s take a look at a panel of different commodities and company profiles. These are designed as introductions, and if something catches your eye, you’ll want to do additional research!

1. Nutrien (NTR)

| P/E | 5.06 |

| Dividend Yield | 2.94% |

| Financials | View |

Nutrien is the largest producer of potash and the third largest producer of nitrogen fertilizer in the world, and the second largest phosphate producer in North America.

The company’s long-term growth prospects are carried by a growing population, growing food demand, and an increasing need for fertilizer to feed the world. It is also benefitting from the disruption of supplies from Russia and Belarus, two very large potash and nitrogen producers.

The company registered a record 2022 year thanks to rising fertilizer prices. It expects this to persist for another year, with more average results in the next 10 years.

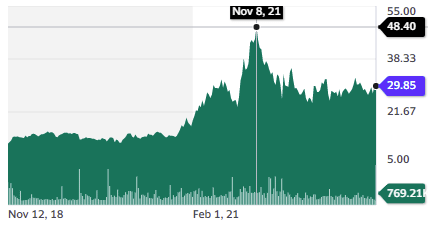

2. KazatomProm (KAP.IL)

| P/E | 9.98 |

| Dividend Yield | 6.06% |

| Financials | View |

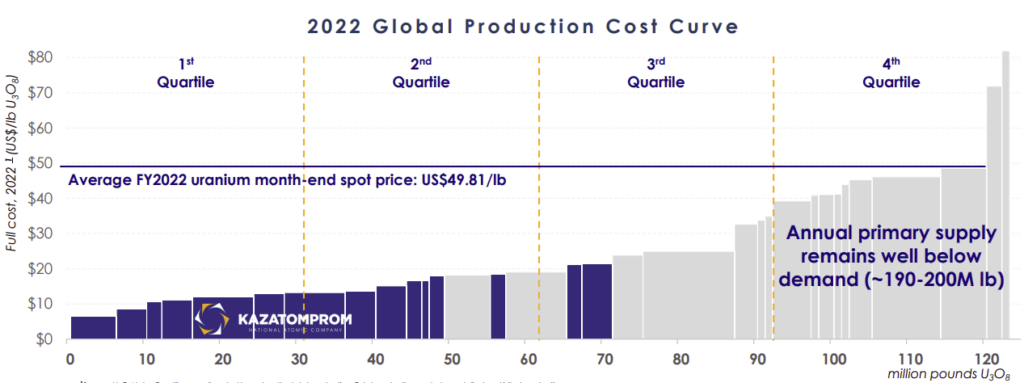

If you’re interested in investing in foreign exchanges, consider the largest uranium producer in the world. Based in Kazakhstan, this company supplies 40% of the world’s nuclear power plants. It has the cheapest production cost of any producer of uranium, owning almost all the cheapest mines in the world to operate.

Due to its cost advantage, Kazatomprom has often been willing to keep uranium prices low enough for long periods to keep competitors out of the market.

Nuclear power is experiencing a renaissance, with the developed world’s unwillingness to stay dependent on energy producers like Russia. The very low carbon intensity of nuclear power is also a powerful incentive.

The main drivers of new nuclear reactor building are China (150 new reactors planned, current total reactor number is just 437) and the emergence of SMR (Small Modular Reactor) as a new and safer nuclear reactor design.

85% of the company is owned by the Kazakh government. It is exposed to geopolitical risks, sharing direct borders with both Russia and China and a coastline on the Caspian Sea (shared by Iran).

3. Rio Tinto (RIO)

| P/E | 9.20 |

| Dividend Yield | 7.09% |

| Financials | View |

Rio Tinto is the world’s third-largest metal miner. Its core assets are Australian iron mines.

Its second strategic asset is Oyu Tolgoi, a copper mine in Mongolia. This mine is currently being expanded and is expected to become the 4th largest copper/gold mine in the world by 2030. Rio Tinto recently acquired all the shares of the project not owned by the Mongolian government, simplifying a complex ownership structure.

It is also active in aluminum, producing this power-hungry metal with hydropower, which insulates the company from global energy costs.

In the long term, Rio Tinto’s large exposure to iron ore will reduce, with more exposure to copper (Oyu Tolgoi) and lithium (including through the recently acquired Rincon project).

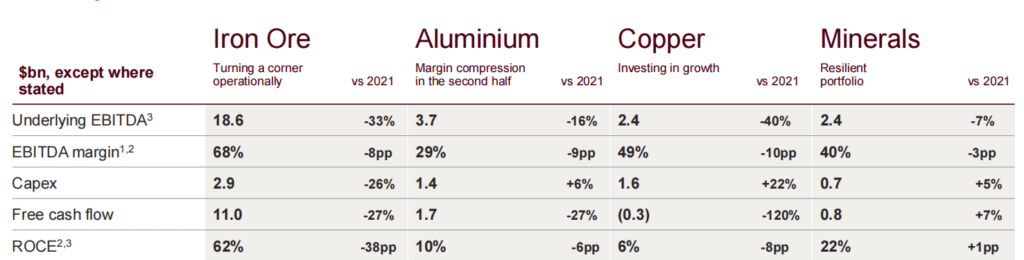

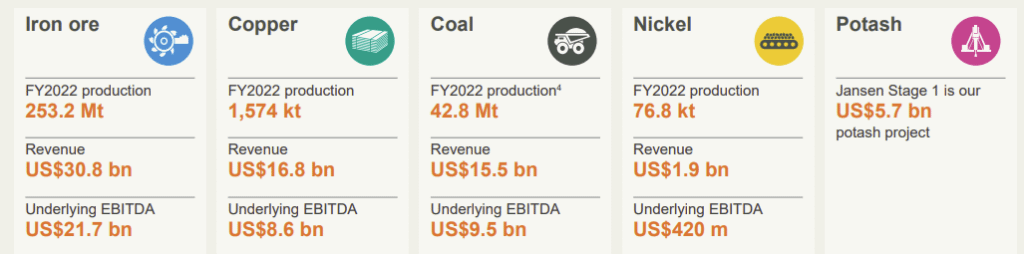

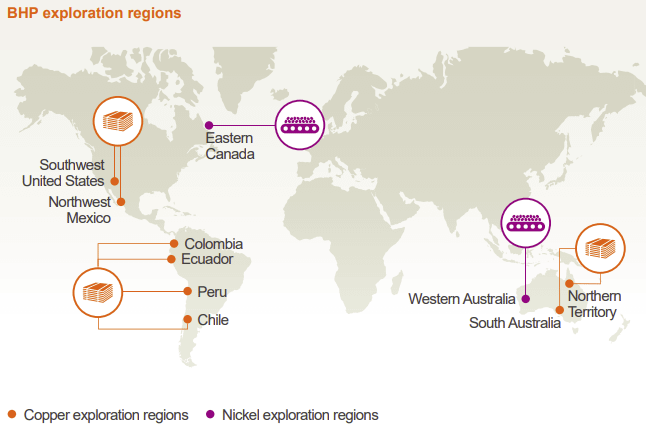

4. BHP (BHP)

| P/E | 8.68 |

| Dividend Yield | 8.79% |

| Financials | View |

This is the world’s second-largest miner, mining iron, potash, metallurgical coal (used to make steel, not for power generation), copper, and nickel. It operates in the Americas and Australia.

The company’s main goal is to develop new copper and nickel mines through extensive exploration. The company is also expanding directly, developing its Jansen potash mine and acquiring Oz Minerals, an Australian copper miner, for $6.4B.

With a presence in copper and nickel, BHP is at the forefront of the growing demand for metals used by the renewable energy industry. Its iron and metallurgical coal is also required for windmills, infrastructure, etc…

It is relatively ESG friendly, with 46% of its electricity sourced from renewables and -25% CO2 emissions since 2021.

5. Sociedad Química y Minera de Chile SA (SQM)

| P/E | 5.60 |

| Dividend Yield | 14.15% |

| Financials | View |

SQM is mostly a lithium mining company with minor activity in the production of iodine and potassium nitrate.

SQM recently boasted record profits, thanks to skyrocketing lithium prices combined with increased production volume. The lithium price increase was supported by quickly accelerating demand, with 2025’s demand expected to stand at 1,500 kMT, double from 2022’s 760 kMT.

The company is a great way to get exposure to the boom of lithium demand for EVs, utility-scale batteries, and other green energy initiatives. It is also vulnerable to any downturn in lithium price, making current high earnings uncertain.

6. EQT Corporation (EQT)

| P/E | 7.50 |

| Dividend Yield | 1.80% |

| Financials | View |

EQT is a leader in shale gas production and the largest single US producer of natural gas, focusing on the Appalachian Mountain region.

The company went through a crisis in 2019-2020, like most shale producers. It is notably marked by negative ROCE (Return On Capital Employed) -7% to -9% from 2019-2021.

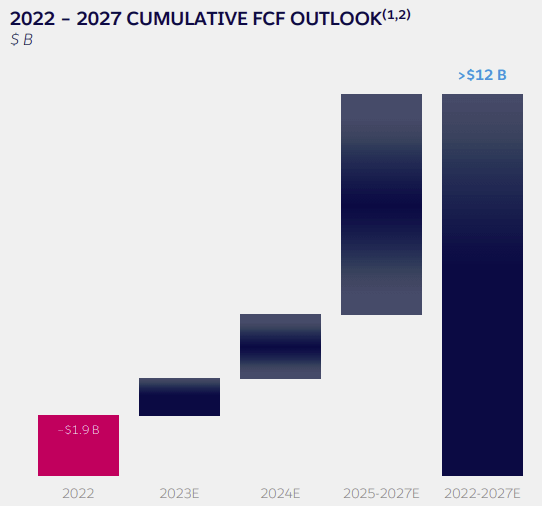

It has since recovered and expects to generate free cash flow equivalent to its current market cap from 2022 to 2027.

The elevated demand for gas (especially exported in the form of LNG) and energy in the US and Europe in the aftermath of the Ukraine war should support EQT in the long term. Still, this is a very volatile market, where one warm winter can collapse gas prices for a whole season.

7. Newmont Corporation (NEM)

| P/E | – |

| Dividend Yield | 3.21% |

| Financials | View |

Newmont is the world’s largest gold mining corporation, with 6 Moz production per year and reserves of 96 million ounces of gold and 16 billion pounds of copper. 90% of these reserves are in the Americas and Australia.

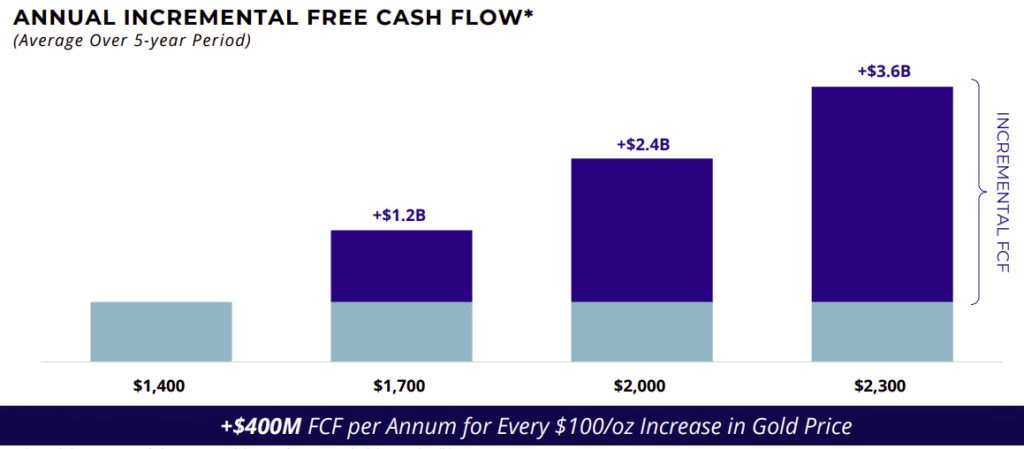

Production is expected to stay stable for at least until 2032. Because of its large reserves and stable production, Newmont is, before anything else, a leveraged bet on gold prices. If gold prices go up, the company’s profit will grow a lot more than the rise in the underlying commodity.

The dividend policy is focused on returning money to shareholders, depending on free cash flow and, thus, on gold prices.

Investors in Newmont might want to hold it as a sizeable bet on a loss of value among major currencies or as a small part of their portfolio, more akin to an insurance policy against black swans events. There’s an old Wall Street saying: “Put 5% of a portfolio in gold, and pray it never goes up”.

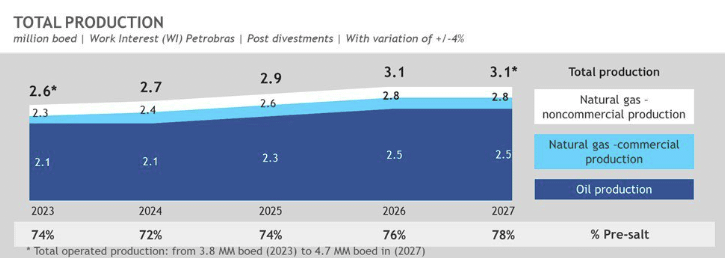

8. Petrobras (PBR)

| P/E | 2.12 |

| Dividend Yield | 65.57% (Not a typo) |

| Financials | View |

Petrobras is the national oil company of Brazil. It produced 2.6 million barrels of oil equivalent per day (boed) in 2022 (roughly 2.6% of the world’s production) and has proven reserves of 10.5 billion boe.

It has recently been out of favor with investors and with a very volatile stock price due to high political risks following the election of the socialist president Lula.

The generous dividend policy combined with a very low valuation has sent the dividend yield in the outstanding 50-70% range. But of course, such dividends will only occur in case the company maintains its policy, an open question with the change of government.

The company also has a significant debt level, even if net debt went down from $79B in 2019 to $41.5B in Q422.

Petrobras is also notable for being one of the oil companies that is most active in drilling for increased production, with its newly appointed CEO declaring: “We may be the last to produce oil in the world.” This contrasts highly with other “Big Oil” firms looking at reducing CO2 emissions and focusing on the green transition.

ETFs (Exchange Traded Funds)

Many prominent commodity-focused companies trade on non-US exchanges, which can be an obstacle for investors who don’t use a broker that allows them to trade foreign stocks. ETFs can address that problem and can provide diversification with even a modest investment.

- VanEck Gold Miners ETF GDX: Top holding is in Newmont, 12.59% of the index, followed by the other largest gold miners.

- Global X Uranium ETF URA: A diversified package of uranium miners and uranium holding trusts.

- Global X Copper Miners ETF COPX: A diversified ETF for copper miners all around the world.

- Energy Select Sector SPDR Fund: A oil & gas ETF focused on US companies.

- iShares MSCI Agriculture Producers ETF: A mix of fertilizer companies (like Nutrien), farming equipment (John Deere), and seed & chemical companies (like Corteva).

- SPDR S&P North American Natural Resources ETF: All major North American commodity producers, including Exxon, Nutrien, Newmont, etc…

- FlexShares Morningstar Global Upstream Natural Resources Index Fund: Diversified international commodities producers, including BHP, Glencore, TotalEnergy, Vale, etc.

Commodity stocks aren’t for everyone. If you’re looking for exponential gains, you’ll want to look elsewhere. If you’re looking for vital overlooked sectors at cyclic lows, commodities might be worth a closer look.

The post 15 Best Commodities Stocks & ETFs In 2023 appeared first on FinMasters.

FinMasters