There is a ton of confusion right now regarding U.S. recessions, as analysts and economists express opposing views on whether the country has entered a recession

Much of the confusion is due to differing definitions of a recession. One widely accepted definition of a recession is when the GDP (gross domestic product) of a country declines for two consecutive quarters. By that definition, the US entered a recession after the 2nd quarter of 2022.

The National Bureau of Economic Research (NBER), which is officially responsible for defining recessions and other components of the business cycle, uses a different definition of recession. The NBER is among the most prestigious non-profit institutions in the U.S. 38 current or former board members have won a Nobel Prize in Economics.

The panel was established to keep politics out of economic data analysis. In order to preserve the autonomy of the council, the economists meet in secret. Former committee member Jeffrey A. Frankel, who served on the NBER for 26 years, said, “The subject of politics never came up once.”

How Does the NBER Define a Recession?

The NBER states that “a recession involves a significant decline in economic activity that is spread across the economy and lasts more than a few months”. How they establish that is a little more complex. One NBER document states that the economists consider “real personal income less transfers, nonfarm payroll employment, employment as measured by the household survey, real personal consumption expenditures, wholesale-retail sales adjusted for price changes, and industrial production”.

The NBER does not announce its conclusions immediately. They wait “until sufficient data are available to avoid the need for major revisions to the business cycle chronology”. In practice, NBER typically takes nearly a year to declare a recession in the U.S. and has never reversed a call.

Bloomberg’s Chief Economist, Anna Wong, said, “The committee’s current methodology is sound. Q1’s contraction is mainly due to strong imports (due to strong demand) after slowdown inventory building due to combination of supply bottlenecks and gangbuster inventory building in Q4 last year. It’s hard to interpret that as a weakness-driven contraction.”

The Current Economic Scenario

One of the major reasons why there is widespread debate about whether the U.S. is officially in a recession is the mixed economic data. The country’s GDP declined by 1.6% in the first quarter of 2022 and by 0.9% (on an annualized basis) in the second quarter. The consecutive decline in two quarters has driven Wall Street analysts to raise recessionary flags.

However, other economic parameters such as labor market data and increased manufacturing activity remain strong. For example, the U.S. economy added 528,000 jobs in July, reaching pre-pandemic levels. The unemployment rate stood at 3.5%, lower than the Dow Jones consensus estimate of 3.6%. An economy cannot have such a strong labor market and be in recession, at least by NBER’s standards.

The U.S. manufacturing numbers increased for the 26th consecutive month in July, indicating strong economic activity. However, the growth rate was slightly lower than in June, indicating signs of a slowdown. In fact, the Purchasing Managers’ Index (PMI) came in at 52.8% in July, marking the lowest reading since June 2020.

What Causes a Recession?

Past recessions in the U.S. have been triggered by a variety of reasons. The 2020 recession was due to the global lockdown resulting in a sharp decline in output. The NBER declared the last recession within a few months since the pandemic outburst in March 2020, as the U.S. GDP and economic activity plummeted sharply, along with 22 million lost jobs.

While the global lockdown triggered a worldwide recession, a sharp decline in output and rising unemployment for several months caused the majority of economies to enter a recession.

However, NBER’s Business Cycle Dating Committee announced that the 2020 recession lasted just two months, making it the shortest U.S. recession ever recorded. Prior to this, the shortest U.S. recession lasted in 1980, which lasted six months.

Recessions can be caused by multiple factors, often interacting, and there’s no consistent rule on what causes a recession.

Major Recessions in U.S. History

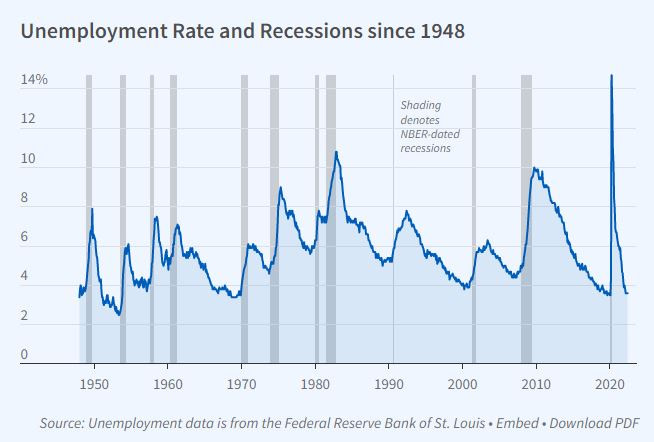

According to the recessions in the U.S. timeline – there have been 11 recessions since 1948. On average, the U.S. has been in a recession every six years, with each downturn lasting nearly 12-15 months on average.

Let’s look some recent U.S. recessions and their causes.

The Financial Crash of 2008

The recession in 2008 began with the collapse of the Lehman Brothers, one of the biggest banks in the U.S. While the Lehman Brothers collapse was the trigger, the underlying cause was a major asset bubble focused on the real estate market and speculation in mortgage-backed securities.

In the early to mid 00s, ultra-low interest rates caused investors to veer toward real estate based on the long-standing expectation that housing prices never go down. Real estate seemed like a highly secure investment to traders burned in the late 90s tech stock boom.

Banks and lending institutions began giving mortgage loans to “sub-prime” borrowers (with poor credit history), albeit at slightly higher interest rates. Inevitably, the sub-prime borrowers began defaulting on the loans. This exposed a much larger bubble in the trading of mortgage-backed securities.

Lehman Brothers, one of the biggest U.S. banks at the time, had immense exposure to the U.S. housing market. When the housing bubble popped, Lehman Brothers suffered extensive losses and eventually filed for bankruptcy.

The collapse of one of the biggest U.S. banks had ramifications on the U.S. economy as well as the rest of the world. This economic downturn, known as the global economic slowdown of 2008, was triggered by the unchecked growth of the U.S. housing market and by the explosion of trading in housing-related derivatives. As the saying goes, “When America sneezes, the world catches a cold.”

In the aftermath of the 2008 recession, several amendments were made to the global financial sector to prevent such a market crash. The Switzerland-based Basel Committee on Banking Supervision rolled out Basel III. The accord has strengthened the resilience capacity of individual banks in case of an industry-wide shock. Under Basel III, banks are expected to maintain substantial capital in hand in order to cushion losses in the event of market headwinds.

The Infamous Dot-Com Bubble

The dot-com bubble was an entirely separate economic phenomenon. Tech stocks were gaining prominence since the late 1990s, causing the Nasdaq Composite index to increase five-fold in just five years. However, the bullish sentiment surrounding tech stocks was not backed by fundamentals, causing the sector to trade at sky-high valuations.

In fact, many of the tech start-ups had no solid business plans and were mere speculative investments. However, these companies spent a fortune on marketing and brand creation to attract investors. At the same time, the rise of online trading platforms brought millions of inexperienced investors into the market. Many of them threw all of their capital into emerging tech stocks. Confidence surged as paper profits mounted, and investors took on more and more risk.

Some start-ups spent up to 90% of their total budget on advertising. The sudden interest of venture capitalists also aided this unprecedented tech growth, as approximately 39% of all venture capital investments were in internet companies by 1999.

However, institutional investors soon began liquidating their portfolio when the Nasdaq crossed the 5,000-mark, as they realized that large numbers of the underlying companies had little hope of churning out profits.

As investors bailed out, speculative tech companies that relied on stock sales to fund operations collapsed. Trillions in investments were wiped out while unemployment levels soared. Thus, millions were left with no jobs and immense losses on equity investments.

Is a Recession Coming? Is One Already Here?

The global economy has come a long way since the decade-long Great Depression of 1929 – the longest and worst recession in modern history. Governments understand recessions better and have learned more about mitigating them (though they don’t seem to have learned how to prevent them).

Today’s macroeconomic scenario does carry unknowns. As in 2001 and 2008, an extended asset bubble is deflating, with prices of growth stocks, cryptocurrencies, and other assets plunging. Post-COVID supply chain disruptions and high commodity prices driven by the Russia-Ukraine war have added the highest inflation since the 70s to the mix.

Will that combination drive a recession? So far, strong employment and industrial production figures have kept the economy out of recession territory – at least by the NBER’s criteria – but nobody’s sure how long that will last. With the Federal Reserve determined to cut inflation by raising rates, which traditionally cools economic activity, there is a real possibility of a recession.

If the economy does sink into an NBER-defined recession, there is one saving grace: historically, a recession is a temporary condition, and the end of a recession typically ushers in a new growth cycle. Recessions aren’t pleasant, but they are an inherent part of the economic cycle, and they do not last forever!

The post Is the US in a Recession? appeared first on FinMasters.

FinMasters