Rising living costs, mounting inflation, and unexpected expenses can leave you short on cash at the end of the month. Cash advance apps can spot your money before your next paycheck arrives.

Unlike other types of loans, cash advances don’t have interest or fees, and they don’t require a credit check. That makes them a great alternative to expensive predatory payday loans. Many also offer other helpful features.

There are some limitations that most cash advance apps share.

- You will have to sign up before you need an advance. Cash advances are only available to members. Many apps charge a monthly fee.

- You must link the app to a checking account where you receive your salary.

- Most cash advance apps use a third-party service called Plaid to connect to your bank account. If your bank or credit union is not Plaid-compatible, finding a cash advance app you can use may be difficult.

- Cash advance apps can get you into the habit of spending money before you’ve earned it.

Within those limitations, cash advance apps can provide a useful service.

Here are the top-five best cash advance apps with annual percentage rates (APR) and fair repayment terms.

Best Cash Advance Apps

- EarnIn –

Besto for large advances

Besto for large advances - Empower – Best for self employed borrowers

- Dave – Best for overdraft protection

- Albert – Best for low-cost banking

- Cleo – Best for budgeting

1. BEST FOR LARGE ADVANCES

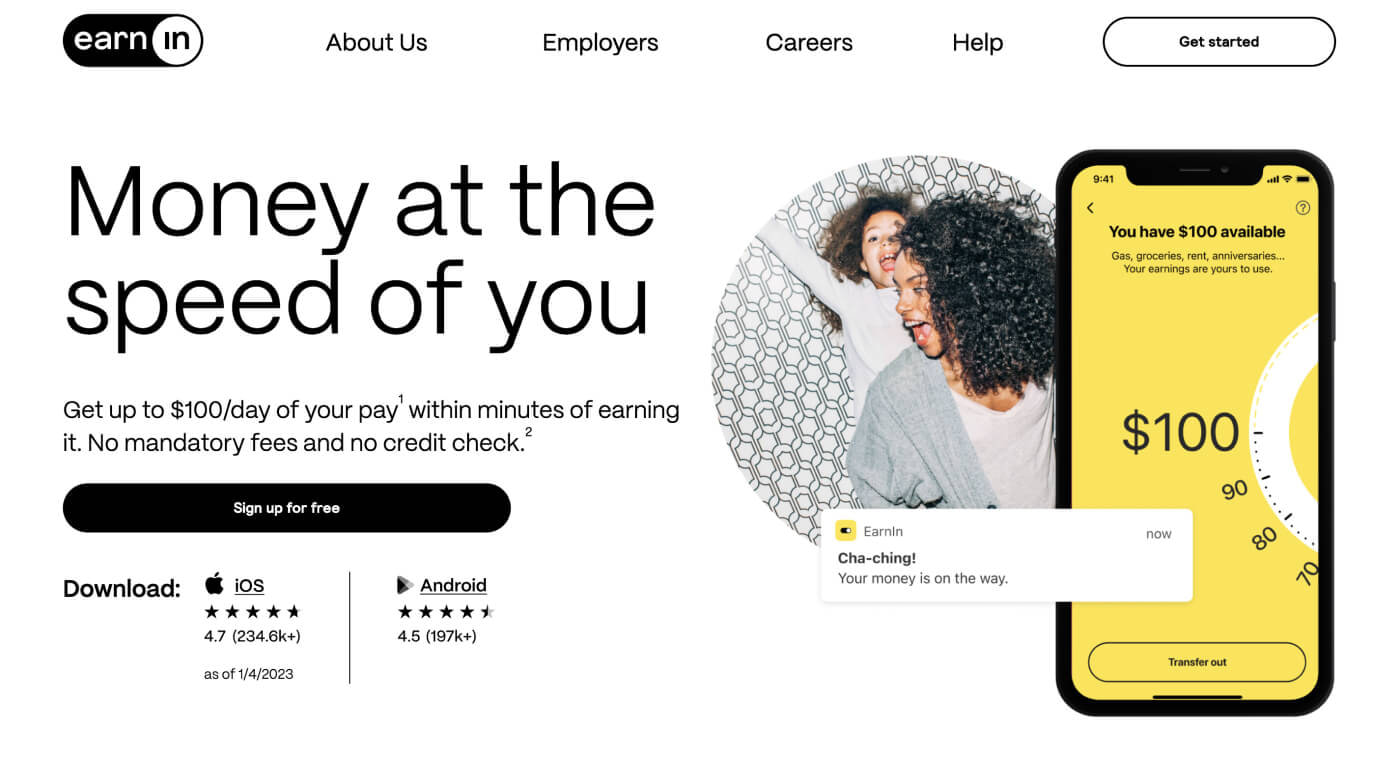

EarnIn

EarnIn offers $100 per day or $750 per pay period (i.e., month) in cash advances against the money you have already earned. There’s a fee for instant funds transfer, and the app will ask for a voluntary tip for each advance.

- Get up to $750 in payroll advance.

- No credit check is required.

- Fast in-app onboarding.

- Same-day transfer to your bank account.

2. BEST FOR SELF EMPLOYED BORROWERS

Empower

Empower offers easy access to cash from its sleek app. To create an account, you must provide only two documents: a valid ID and current proof of address. Once you’ve linked a checking account, you can instantly verify your availability for an advance without providing other employment records.

- Up to $250 in instant cash advance.

- No employment verifications are required.

- Free debit card with cashback.

- Extra in-app budgeting tools.

3. BEST FOR OVERDRAFT PROTECTION

Dave

Dave protects you against costly account overdraft fees by monitoring your spending and alerting you whenever you’re about to hit a negative balance (because of upcoming bills). To help you out, Dave spots you cash until the next paycheck arrives.

- Up to $500 in instant cash advance.

- Automatic budgeting features.

- Payback in installments is available.

- No late or minimum balance fees.

4. BEST FOR LOW-COST BANKING

Albert

Albert meshes essential banking services with payday advances. You get a free debit card, an FDIC-insured savings account, and an affordable investing app with an AI financial management assistant (for a separate membership fee).

- Get up to $250 in instant cash.

- Get your full paycheck up to 2 days early.

- Up to 0.10% annual bonuses on all savings.

- Micro-investments in stocks from $1.

5. BEST FOR BUDGETING

Cleo

Cleo is a personality-packed financial app combining cash borrowing with other money-management features such as a credit building product and AI-driven budgeting tools. With Cleo, you can spot money and learn how to manage your cash flow better.

- Up to $100 in an instant, no-fee advance.

- Two-minute sign-up process.

- No proof of employment is needed.

- Free ACH transfers to a linked bank account.

EarnIn

EarnIn is a single-purpose cash advance app. It lends you money against your future paycheck at no cost. EarnIn doesn’t require a credit check.

The app is primarily designed for full-time salaried employees. To qualify for an advance, you must be of legal age, legally reside in the US, and provide employment information. Also, you must link a checking account (savings or prepaid accounts are not accepted).

To qualify, your salary must be direct-deposited into your checking account. EarnIn will verify this to ensure your eligibility.

As part of onboarding, you’ll have to prove your wage by uploading employer-issued timesheets, adding a valid, employer-provided work email, or adding a complete work address and keeping your GPS on for the app to verify your work hours (aka the time you spend at the designated address).

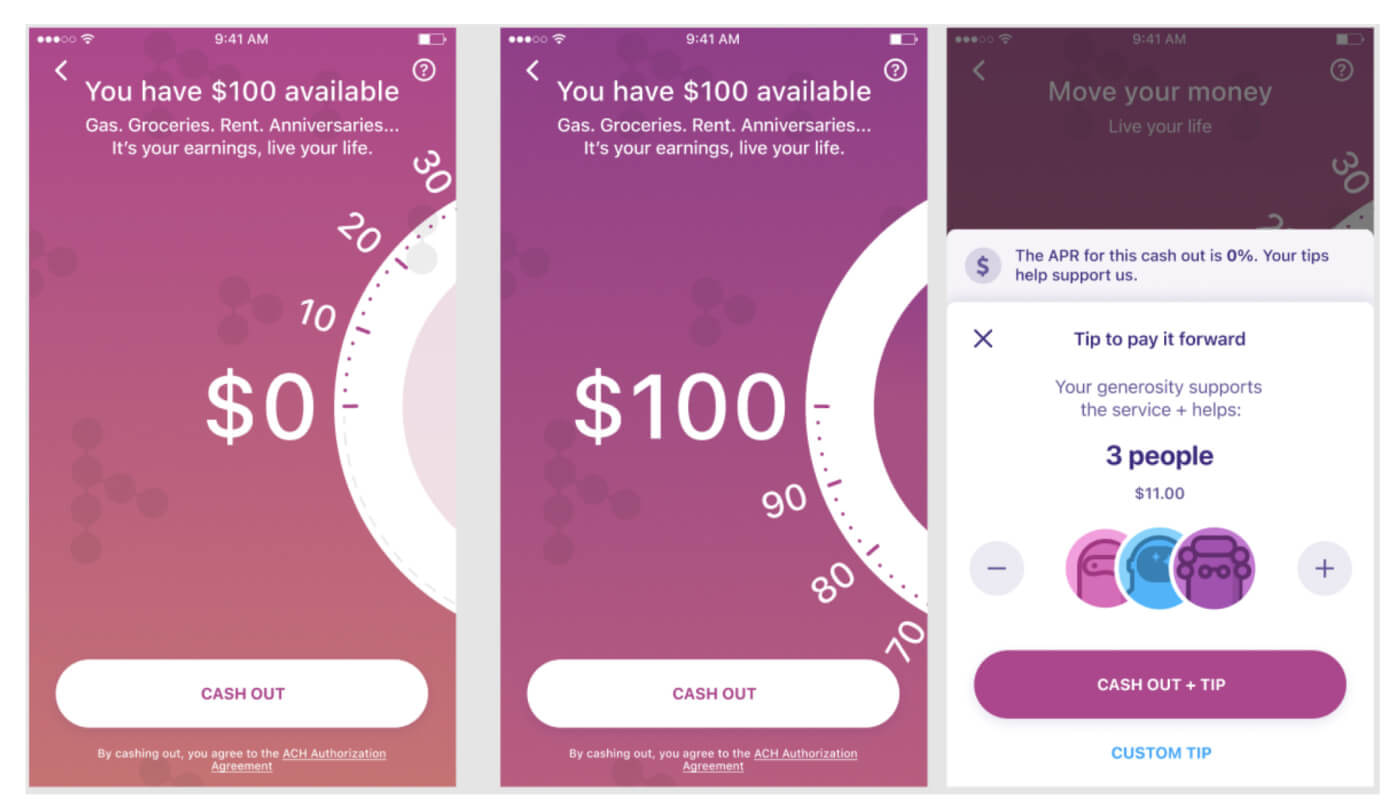

EarnIn then takes 2-3 business days to verify the provided information. Once verified, you’ll get instant access to your free cash advance. You can add a custom tip amount (optional) to support the company.

Source: EarnIn.

You can withdraw cash to a linked debit card or a bank account. ACH withdrawals are free but take 1-3 days to process. For instant fund transfer, you can pay an extra $0.99-$3.99.

When your next paycheck is deposited to your linked bank account, EarnIn will debit your cash advance, instant processing fee, and tip amount (if any).

Pros

Pros

- The highest paycheck advance of any cash advance app

- No monthly fees for using the service

- Low express fee for same-day payouts

- Unlimited cash withdrawals on EarnIn card

- No credit check

- Top-notch account security and personal data protection

Cons

Cons

- Your salary must be direct deposited to your linked bank account

- Mandatory timesheet/worksheet submission

- Self-employed people don’t qualify

- Tips can add up to a substantial amount

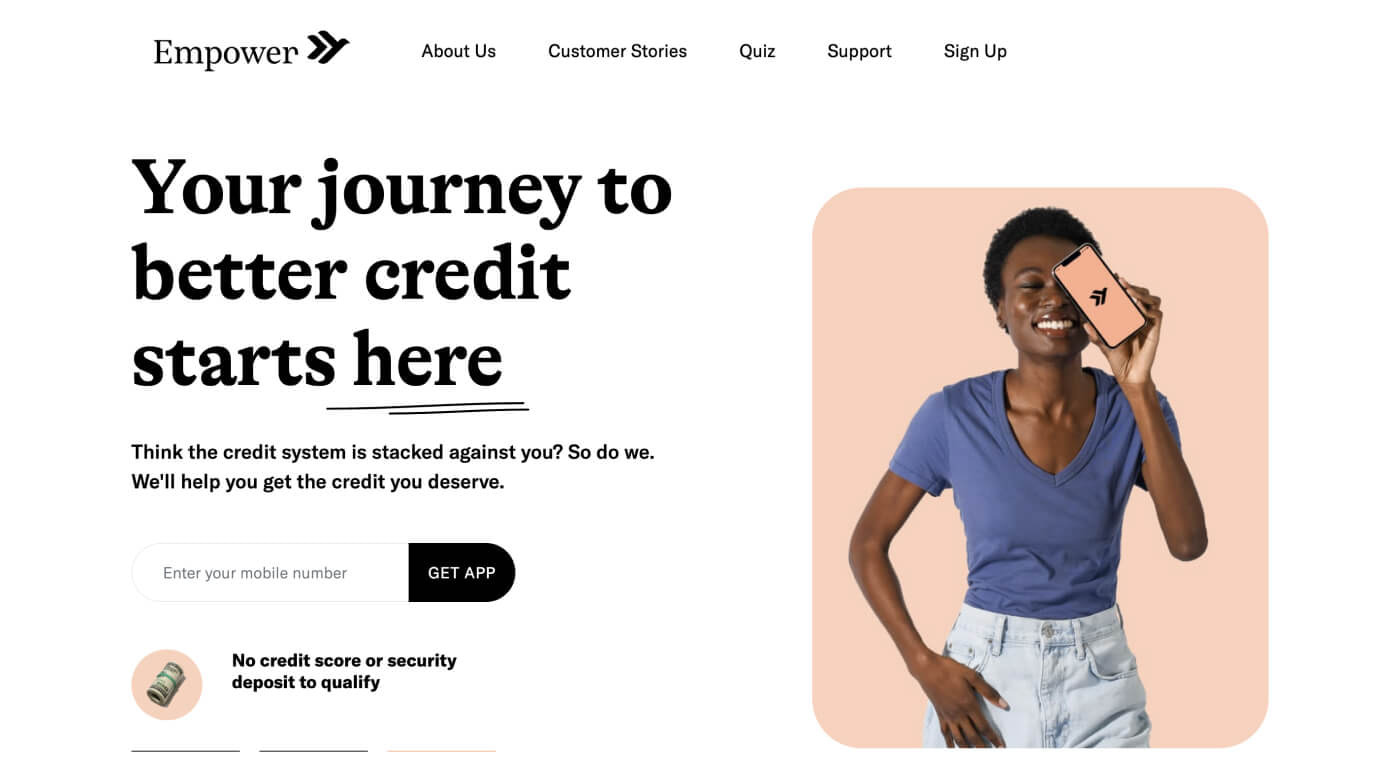

Empower

Empower positions its cash advance app as an alternative to traditional personal loans (which require good credit) and predatory payday loans. The company has issued over $500 million in advances.

With Empower Cash Advance, you can get up to $250 with no interest, no late fees, and no credit checks. Unlike EarnIn, Empower charges an $8/month subscription fee to borrow money and access banking features.

For that price, you also get a no-fee debit card, offering up to 10% cashback. If qualified, you can access your paycheck two days earlier or receive a free instant advance payout. Otherwise, same-day advance delivery to a linked bank account costs $1-$8.

To open an Empower account, you must provide a valid ID document and proof of address no older than 60 days. It can be a pay stub, a utility bill, an official bank statement, or a lease agreement. If you’d like to open an Empower bank account and get a debit card, you must provide your Social Security number. Then you’ll need to connect a checking account where you receive regular direct deposits.

Empower doesn’t verify your employment history like other popular cash advance apps. If you’re self-employed or do gig work, you’re still qualified to get a cash advance.

Once your account is activated, go to the Cash Advance section on your Accounts tab and click “Check eligibility” to check if you qualify for an advance. The app will automatically tell you how much money you can borrow. The results are instant. To increase your advance limit, repay the sum on your next payday and carry a positive balance in the connected bank account.

The app will only advance the amount you are approved for. You can’t borrow less.

To increase your advance limit, repay the sum on your next payday and maintain a positive balance in the connected bank account.

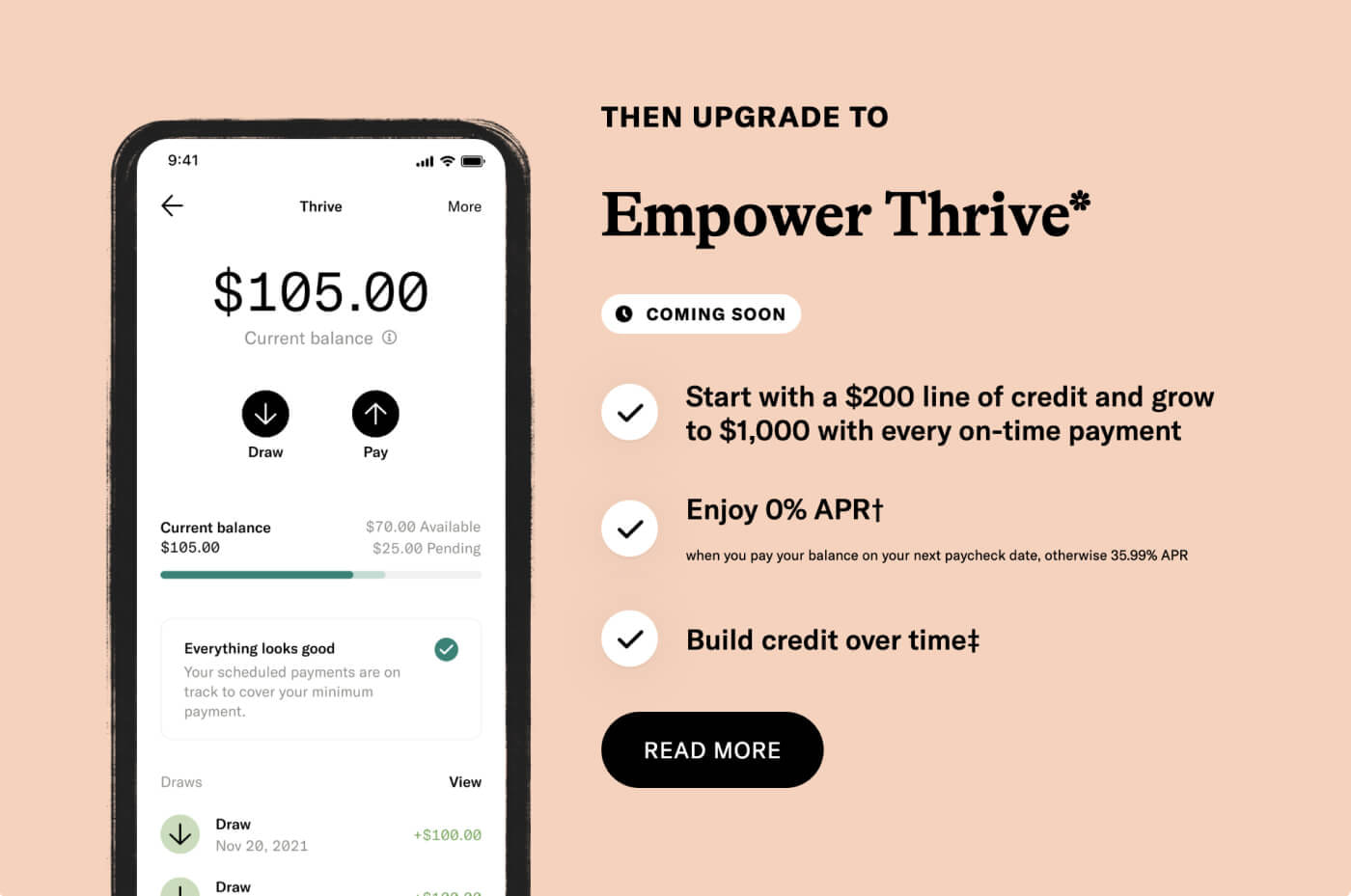

Empower also has a new lending product called Empower Thrive, a line of credit that is reported to the credit bureaus and can help you build credit.

Promising a higher credit line (up to $1,000), Empower Thrive can be a more affordable alternative to high-interest personal loans. But it comes with more strings attached, including a 35.99% APR if you miss a payment. Also, you’d be subject to a credit check.

Pros

- Simple account registration process

- No employment information required

- Instant lending decisions

- Free debit card with cashback offers

- Access to AI-driven saving tips

- Monthly income and expenses report

Cons

- Charges a monthly membership fee

- Doesn’t allow you to choose a lower cash advance amount

- High APR rate for a credit building product

Dave

With Dave, you can receive up to $500 at once, which is more than most cash advance apps offer. You can get access to your paycheck up to two days early if you’re a salaried employee. The average approved advance new users get is $120.

You can transfer the money to an external account for free. Transfer time takes 1-3 business days. You can also transfer your money instantly to a Dave payment account for free or get an instant payout to a connected debit card or bank account for a fee ($2.99-$13.99).

While Dave doesn’t do any credit checks, it analyzes your transaction history in connected bank accounts to determine income and spending habits. To get a higher payout, you should demonstrate good financial management.

Your bank account should also have at least three monthly recurring deposits totaling $1,000+. Dave will check for any recent negative balances on your account in the last 60 days. You don’t have to provide proof of employment to access a cash advance.

Dave also offers more flexibility in loan settlement than other cash advance apps. By default, your repayment date is set to the next payday. If your account balance is still low, Dave will collect partial settlements until the full sum is paid. No late fees or interest rates apply.

To use Dave’s cash advance feature, you’ll have to pay a $1 monthly membership fee, one of the lowest fees of any fee-bearing cash advance app. You’ll also get access to budgeting tools, at-risk of overdraft fee notifications, and survey-taking side gigs.

Pros

- Flexible settlement date, no late fees

- Avoid overdraft fees with timely notifications

- Progressively increasing cash advance limit

- FDIC-insured spending account through a partner bank

- Free debit cards with up to 15% cashback

- No cash withdrawal fees in 37,000 ATMs

Cons

- High instant transfer fees to an external bank account

- Short repayment terms (7 days) without extension

- Slow customer support, according to user reviews

Albert

Albert is not a bank, but it offers most of the features traditional financial institutions do, and for a lower cost. Albert has several products rolled into one. You can receive a direct deposit and spend the funds using a free debit card. Separately, you can (and should) link up other bank accounts to benefit from Albert’s money-saving features. The app will help you monitor upcoming bills and suggest actionable ways to lower them (either by negotiating or switching to another provider).

You can also open a free savings account powered by a smart saving algorithm. It monitors your spending and income to predict your monthly account balance fluctuations. Then it automatically transfers small savings amounts to your rainy day fund. Users get a 0.10% bonus (or 10 cents for every $100) in their savings account over a year.

Albert Instant is the cash advance feature available to all Albert users (free or premium). A premium Genius tier costs $8/month minimum. You must activate a 30-day free trial to apply for a cash advance. You can cancel your subscription without losing access to advances (but some other banking and investment features won’t be available).

Albert offers cash advances of up to $250 at a time to all eligible users. To qualify, you must connect a checking bank account where your income is regularly deposited. The connected account(s) must not carry a negative balance over the past two months (i.e., have no history of overdraft fees), and it must have transactions indicating consistent income from the same employer. That makes Albert a less attractive option for self-employed professionals.

Also, you may not qualify for an advance if your paychecks arrive late or have been withdrawn from your account in less than 24 hours.

On the positive side, qualified candidates can get a cash advance of $250 three times within one pay period, if they’ve successfully repaid the previous one.

Pros

- Up to $250 in one-time advance or $750 max per pay cycle

- No credit checks or employment verification documents

- Access your full paycheck up to 2 days in advance

- Request free consultations from financial experts as a Genius member.

- Optimize your spending with automatic budgeting and bill management tools

- Start building your wealth with micro-investments in stocks and mutual funds

Cons

- Premium subscription trial activation is required to apply for Albert Instant.

- A longer list of qualification criteria to max your cash advance size.

- Borrowing money against future earnings may become a habit.

Cleo

Cleo lets you borrow money without providing many documents. First-time borrowers usually qualify for a $20–$70 cash advance. You can get as much as $200 after a successful repayment.

This cash advance app functions as a conversational chatbot. An in-built AI assistant monitors your transactions, then proactively suggests when and how to trim your spending to meet your saving goals.

To qualify for an advance, you must be a Cleo Plus user. The monthly membership fee is $5, but for that price, you also get access to other financial products like a useful budgeting app and a free credit-building tool.

To register a Cleo Plus account, you must provide a copy of your ID and proof of address. Once these are verified, you’ll get access to all account features: budgeting dashboards, spending tracker, cashback, and cash advances. To get the most out of Cleo, you’ll need to link one or more existing bank accounts.

Cleo doesn’t ask for any employment history records or W2 forms. But to get a higher cash advance, you’ll have to actively use their product. That means connecting bank accounts, providing details about your income, and setting up at least one budget.

In other words, the app nudges you to exercise more financial diligence and build good money habits, which is a great advantage.

Pros

- Fun and engaging budgeting tools

- Witty and smart personal finance coaching

- Amazing app design

- No employment records required

- Access to credit builder loans

- Automatic round-ups for savings

Cons

- A monthly membership fee applies

- Low cash advance limit

- No free debit card offered

The Best Cash Advance Apps Compared

| EarnIn | Empower | Dave | Albert | Cleo | |

|---|---|---|---|---|---|

| Eligibility criteria | You have to be a payrolled employee whose paycheck is directly deposited into a bank account. | You must have a US bank account, proof of address, and phone number. Also, you must have two deposits in your bank account of over $200 in the last three months. |

You must link a bank account that is at least 60 days old. You must have received at least 3 recurring deposits in it. |

You must hold a bank account with a US financial institution. Your balance must be above $0 for at least two months. The same employer has paid you consistently for the past two months. After receiving your last paycheck, funds remain available for at least 24 hours |

You must have a US bank account, an SSN, and a recent proof of address. |

| Cash advance limits | $100 per day $750 per pay period. |

$250 per pay period. | $500 per pay period. | $250 one-time advance Up to 3 times per pay period. |

$100 per pay period. |

| Credit check | None | None | None | None | None |

| Supported OS | iOS and Android | iOS and Android | iOS and Android | iOS and Android | iOS and Android |

| Deposit speed | 1-3 days for standard transfers. Same-day for Lightning Speed transfers (cost $0.99 to $3.99). |

1-3 days for standard transfers. $1-$8 fee for an instant top up. |

1-3 days for standard transfers. $1.99-$9.99 express fee for Dave checking account holders. $2.99-$13.99 for express transfers to other banks’ accounts. |

2-3 days for standard transfers. $3.99-$6.99 for any advances made to a linked debit card. |

1-3 days for standard transfers $3.99 for express (same-day) transfer. |

| Subscription fees | No | Yes $8 monthly subscription fee. |

Yes $1 monthly membership fee. |

Yes From $8/month |

Yes $5.99 a month |

| Employment verification required | Yes | No | No | Yes | No |

| Repayment terms | Withdraws cash from your bank account on your next payday. | Automatically takes money from your account based on the pay cycle the app detected. | The default advance settlement date is set to either your next payday or the nearest Friday from when you took an advance. Users can request an extension or allow partial settlements. |

Attempts to withdraw repayment on the day of your direct paycheck deposit. If your repayment is 15 days or more overdue, Albert will suspend your use of Instant for 30–90 days. |

Flexible. You can choose a repayment date — anywhere between 3 and 28 days. |

| Bank account requirements | Any US checking account in your name with a connected debit card Prepaid and pay cards aren’t accepted. |

Any bank account with a U.S. financial institution. You can also withdraw funds to an Empower bank account with a linked debit card. |

Any US regular checking account in your name. Or you can open a free checking account with Dave to benefit from its budgeting tools. |

Any US regular checking account in your name Or you can open a free money account with Albert to use other features. |

|

| Extra services | None | Free debit card with cashback. Automatic savings from each paycheck, deposited with Empower. Spending reports and alerts about upcoming bills. |

Free debit card with 15% cashback. Spending account with no minimum balance fees. Automatic budgeting tools. Earn extra cash by participating in surveys. |

Free checking account and no-fee debit card. Early access to your paycheck (for salaried employees). AI-driven financial advisor and access to human experts. Invest from just $1 into popular stocks. |

Credit history building product Personalized budgeting plan Monthly bill payments tracker AI-driven saving tools. |

| Does Your bank need to be compatible with Plaid? | Yes | Yes | Dave uses Plaid or Galileo. | Yes | Yes |

Should You Use an Advance App?

Cash advance apps can be useful. If a cash advance app keeps you from having to rely on a predatory payday loan or title loan, it’s done its job, and you’ve come out ahead.

Cash advances also carry risks. When you take a cash advance, the app pays itself back from your next paycheck. That leaves you with less money for your next pay period and makes it more likely that you’ll take on another loan.

Relying on a cash advance once in a while when things go wrong is not a problem. If you’re becoming dependent on cash advances and using them every month, something is wrong with your money management, and you need to do something about it.

Cash advances are not a substitute for good money management. Effective budgeting, living within your means, and building an emergency fund is still necessary.

Most cash advance apps come with other tools that are designed to help you budget and manage money. You’re paying for those tools, so you should use them!

The post 5 Best Cash Advance In 2023 to Get Fast Access to Cash appeared first on FinMasters.

FinMasters