Vietnam has been an uninterrupted growth story since the early 1990s and it’s still going strong. This reflects the inherent strength of the country from an economic and human capital point of view.

Nevertheless, it started from such a low point, after decades of devastating wars, that the country still has a lot of catching up to do. It is now moving up the supply chain and could be an early beneficiary of the USA-China tensions and the diversification of international supply chains.

Vietnam Overview

Vietnam is a country of 99 million people and a GDP of $469B ($1.4T in PPP), giving it the 15th largest population in the world and the 36th largest economy (26th by Purchasing Power Parity).

The country has traditionally been mostly agrarian, relying on advanced irrigation systems and a very warm and wet climate, ideal for rice farming.

Except for its impressive agricultural production, especially rice, the country is relatively poor in natural resources, with just a little bauxite (aluminum ore) and oil, mostly used domestically.

It mostly follows the South China Sea’s western coast, with a mountainous interior and 2 major river deltas: the Red River Delta in the North and the Mekong River Delta in the South.

The country was scarred by the fallout of the Indochina War (with France: 1941-1954), the Vietnam War (with the USA: 1955-1975), and even a brief fight with China in 1979.

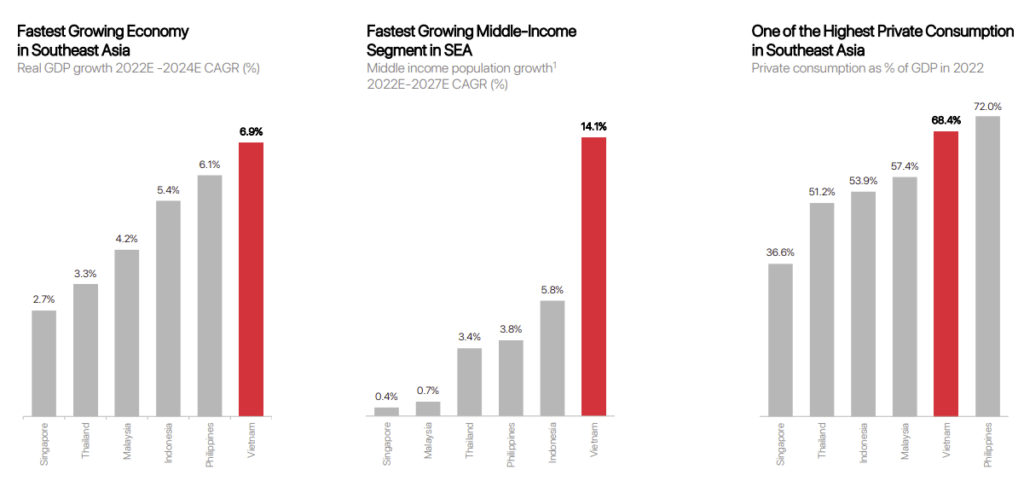

The country’s first burst of growth came in 1990-1997, with 8% annual growth, following free-market reforms. It would, later on, slow down during crises, like the 1997 Asian financial crisis, then in 2000 and 2008. Overall, the country has sustained steady economic growth over that time, with an annual growth rate usually in the 7% range.

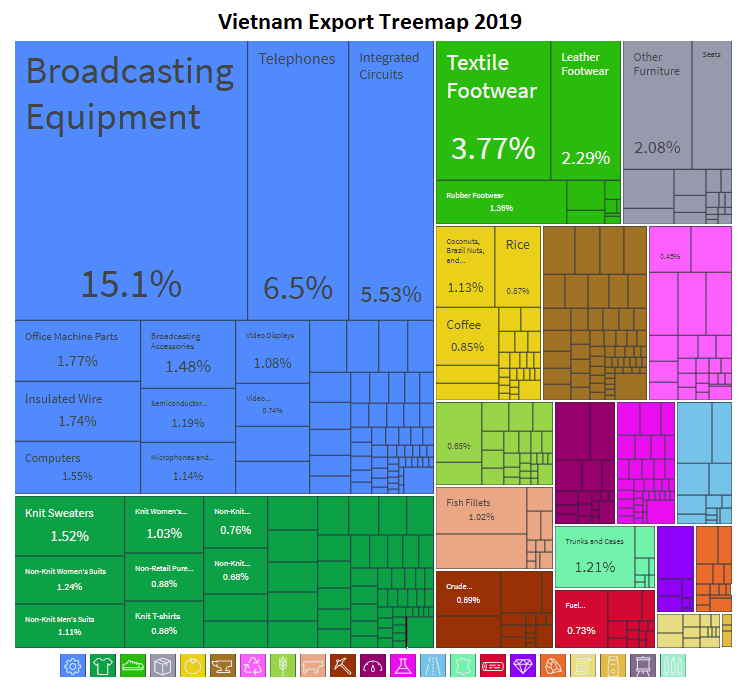

The main export is electronic & telecom equipment, often assembled in Vietnam to leverage the still relatively low labor costs, which became increasingly competitive as China became less and less cheap. The next largest export categories are clothing, footwear, furniture, and food products.

Tourism is also an important part of the economy (7.5% of GDP), or at least was before the Covid pandemic, with the large majority of tourists coming from Asia.

Vietnam has often been categorized as one of the “Tiger Cubs” (essentially the ASEAN), in reference to the previous 4 Asian Tigers (Hong Kong, Singapore, Taiwan, and South Korea).

The Tiger Cubs club has seen growth decelerate strongly in the last few years, with the exception of Vietnam, which is by far the best performing of these economies.

Vietnam’s Strengths & Future

Vietnam’s growth has been fueled by a few factors:

- It is located in Asia, close to most international supply chains.

- Labor costs are low and quality is relatively high.

- The economy has become very open.

- Vietnam has a young and growing population.

- The politics are stable and the environment is safe.

While these advantages still hold, the progressive development of the country makes them less crucial for the next step of Vietnamese development. The demographic transition is happening and salaries are rising. Luckily, the growth is supported by 2 new trends.

Going Up the Supply Chain

Following the blueprint established by Japan, South Korea, and China, Vietnam is now looking to become more than a mere assembler of goods manufactured somewhere else, or the maker of low-value and labor-intensive goods like clothing.

For example, it has become a key supplier to foreign firms for car parts, for a total of $4.4B in car parts exports in 2018.

West-China Tensions

Despite their “tense” common past, Vietnam is surprisingly friendly to the USA, seeing it as a counterbalance to an increasingly powerful and influential China.

Vietnam has been one of the prime beneficiaries of factories leaving China, looking for both cheaper labor and lower geopolitical risk.

The most likely scenario is for Vietnam to climb the supply in segments that are not too labor intensive, as its much smaller population, relatively well educated, is unlikely to be enough to absorb labor-intensive industries currently dominated by China (which is a role that India fits better).

Vietnam’s Weaknesses

One key Vietnamese weakness in keeping growth stable and absorbing more of the added value is that most of its exports are currently controlled by foreign firms. They might set up shop in Vietnam, but they do not replace local champions.

Local firms are generally not up to the level of quality required to become independent suppliers. This might change over time, as more of the labor force is gaining experience, skills, and connections to start on their own. It is still just a (distant?) possibility for now.

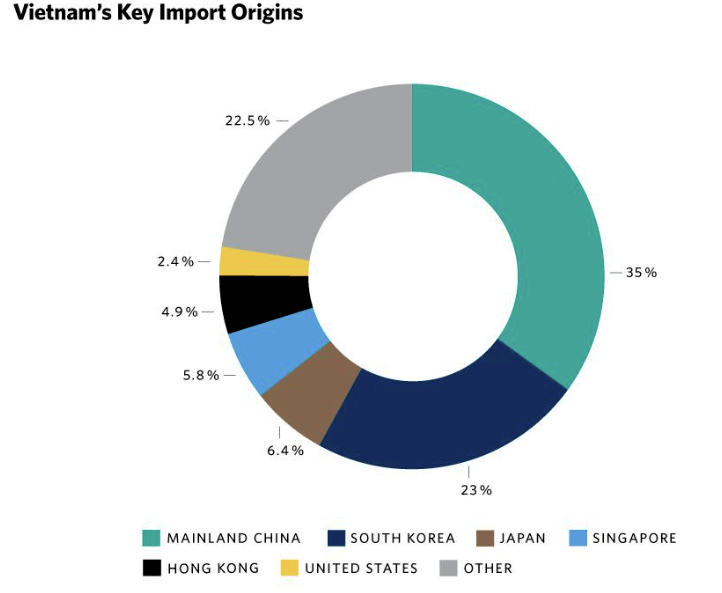

Another key weakness is dependence on China. China provides 35% of Vietnam’s imports. So when people look at Vietnam as an alternative to China, they might underestimate how much Vietnam functioning properly relies on keeping at least decent relations with China.

The last issue is that Vietnam needs to invest more massively in its infrastructure. Power demand has often caught up to max capacity, and the same can be said for logistics infrastructure (roads, railways, harbors). Strong investments by the government and local utilities will be needed, especially if the country moves toward more energy-intensive industries.

Company Spotlights

Vin Group (HOSE:VIC)

Vin Group is THE conglomerate of Vietnam and the closest the country has to a Korean chaebol (Samsung, LG, etc.) or a Japanese trading company. It represents around 12% of the main Vietnamese stock index (VN-Index) and 1.1% of the country’s nominal GDP.

The company has an interesting history, having been founded by Vietnamese expats in Ukraine in 1993, before being brought back to Vietnam in 2000.

It is mostly active in real estate development and asset management (shopping malls, hotels, condos, etc.), but is also operating data management, wine selling, hospitals, university, and even manufacturing its own design of e-motorcycles and electric cars (VinFast, expected to IPO in 2023) and AI.

Due to this very diversified array of activities, the Vin Group is present in the daily lives of most Vietnamese. With its deep pockets, it is also one of the best candidates for real domestic innovation and taking control of industrial supply chains.

SABECO – Saigon Beer Alcohol Beverage Corp. (HOSE: SAB)

P/E: 20.35

Dividend yield: 2.11%

The 148-year-old company is dominating the local beer market. Considering how beer brands successfully keep out foreign competitors, this is a rather “moaty” business. Vietnam is also, surprisingly maybe, a “beer country”, with beer accounting for 90% of alcohol sales.

The company’s sales and profits have fully recovered from the Covid slump. The company is also investing heavily in its physical assets (breweries, automation, etc.) and its brand (sponsorship of the national football team, music festivals, etc.).

With rising national income, SABECO is well-positioned to capture an increasing budget on entrainment and consumption. SABECO’s management also anticipates increasing consumption from women and young people.

GEMADEPT (HOSE:GMD)

P/E: 17.36

Dividend yield: 2.2%

Gemadept dominates the port operation and logistics businesses in Vietnam, a crucial role in a trade-dependent economy. It is well-positioned to gain from any increase in imports and exports.

It was among the first 3 companies to be privatized in 1993 and was publicly listed in 2002.

Due to its crucial role in the logistical chain, Gemadept essentially acts like a toll charge on the whole Vietnamese industrial sector. Its harbors are unique assets virtually impossible (or at least horribly costly) to replicate, especially the deep-sea harbor that opened in 2021.

More recently, the company has also gotten involved in real estate, with the development of a commercial center, offices, and a 5-star hotel, for a total investment of $280M.

ETFs

While Vietnam is usually included in Asian or ASEAN ETFs, there are a limited number of ETFs centered exclusively on the country.

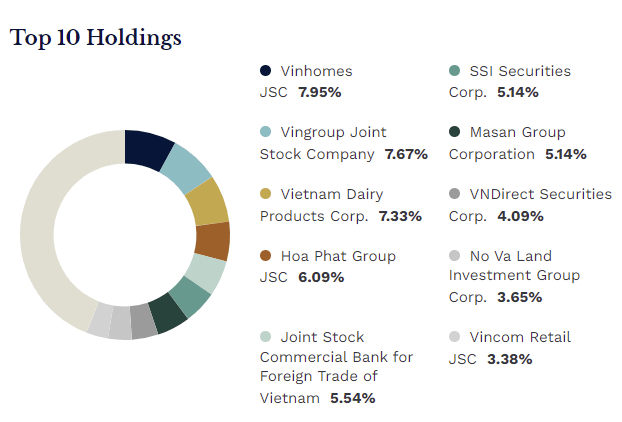

VanEck Vietnam ETF (VNM)

Heavily tilted toward Vin Group and its subsidiaries, it also has a lot of exposure to the financial sector (51% of the whole ETF) and consumer non-durable goods (19%) sectors (partly through Masan Group Corporation, a retailer/supermarket chain).

So this might be a suitable ETF to bet on Vietnam’s overall growth, but only as long as the Vin Group is doing well.

MSCI Vietnam ETF (VNAM)

The ETF top holdings are not very different from VNM, except for a larger exposure to real estate through Hoa Phat Group (9% instead of 6%). It is also more exposed to raw materials and energy.

Conclusion

Vietnam is a growth story that has not disappointed in the last 30 years.

Vietnam might, at this point, be a place where it is relatively easy to invest (no longer a frontier market, with exposure through ETFs) but with a lot of growth potential remaining.

It seems on the verge of starting a new chapter, looking to become a new South Korea or Taiwan in the next few decades. This lofty goal is achievable if the country manages to play its cards wisely and use geopolitical tensions to its advantage, but avoid getting caught in an actual conflict in the South China Sea.

A deep understanding of competitive advantages and local markets might be required for optimal stock picks of Vietnamese small caps. But the country’s blue chip companies offer “simpler” opportunities as well, with large conglomerates, logistic companies, or consumer goods giants and retailers.

Finding Value in Emerging Markets

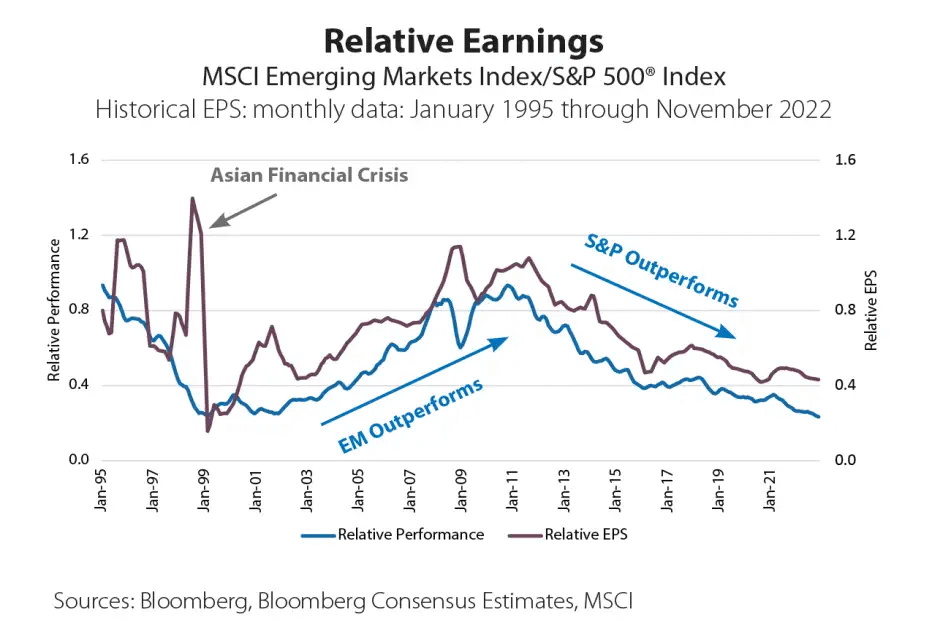

Stock Spotlight has regularly covered stocks in emerging markets, which can offer great companies at discounted prices. After a decade of outperformance for the US stock market, it might be time for emerging markets to shine. This cycle between emerging market (EM) vs the US tends to be roughly 10-15 years long, as you can see below. With the S&P500 outperformance stated in 2010, we are due for a reversal in trend.

Source: Western Southern

Past patterns may not be repeated, but the investing world extends beyond the US, and increasing numbers of investors are considering exposure in non-US markets!

Emerging Value

This is a series focused on opportunities in emerging markets. The goal is not to discuss breaking news. Instead, we will focus on long-term trends and lasting phenomena that will impact investing in a country or region. It will also look at a selection of companies that might be worth a closer look.

The post Emerging Value: Spotlight on Vietnam appeared first on FinMasters.

FinMasters