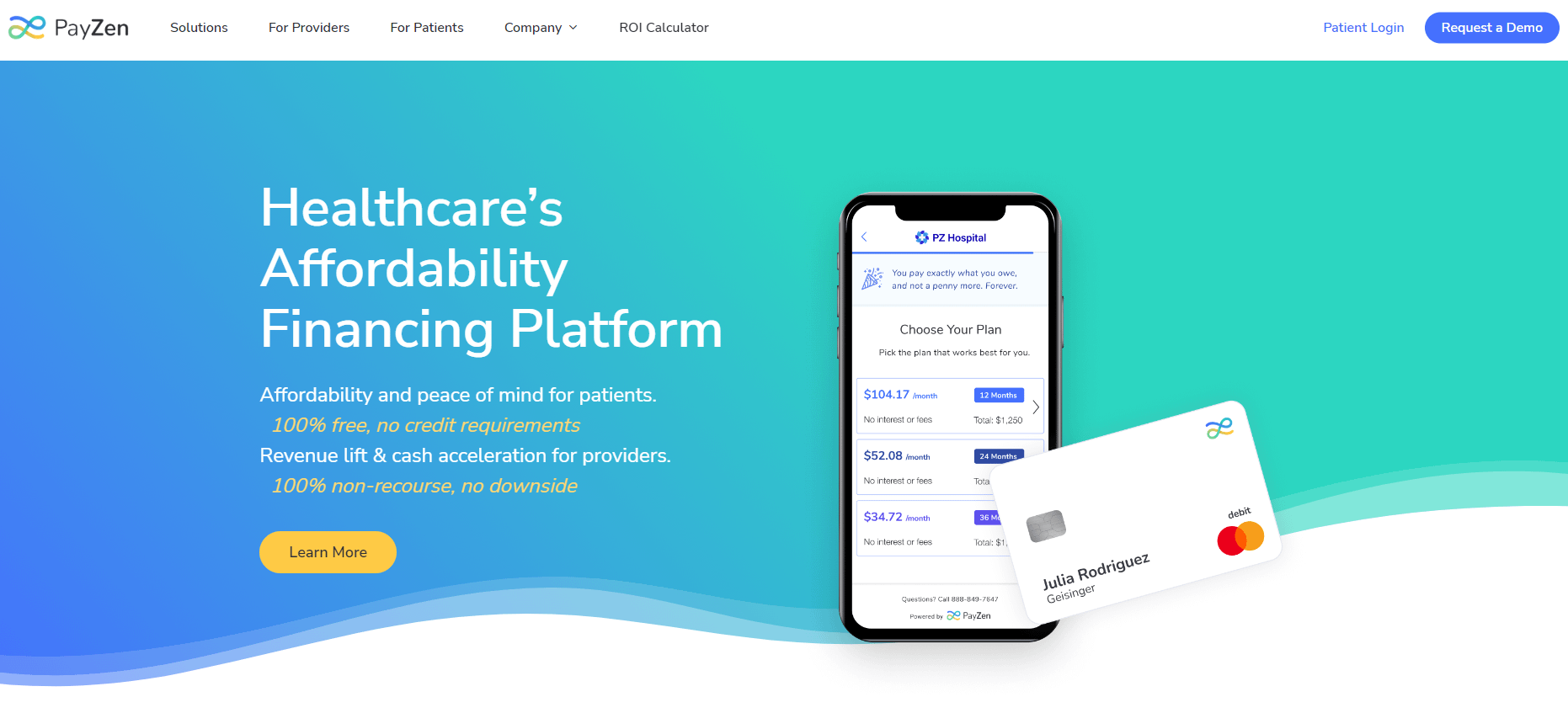

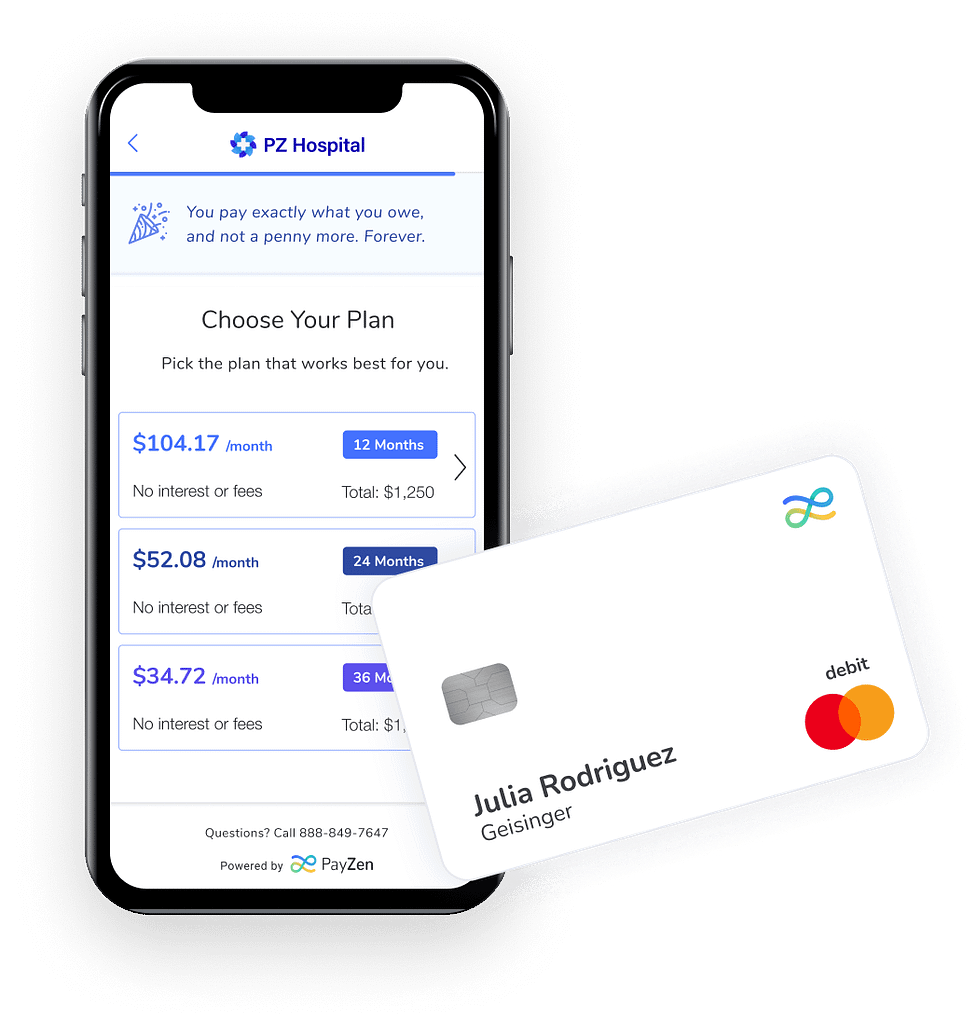

PayZen is a startup company that has set its sights on one of America’s most pressing problems: medical affordability. The solution is simple. PayZen pays your bill and offers you an affordable payment plan with no interest or fees.

But how is that possible? With no interest and no fees, how does the company make money?

To answer that question, we have to take a closer look at the healthcare affordability crisis.

Note: do not confuse PayZen, the healthcare financing system, with the PayZen payment processing app.

Note: do not confuse PayZen, the healthcare financing system, with the PayZen payment processing app.

Healthcare: The Unaffordable Dream

100 million Americans have medical debt[1]. Families are liquidating retirement savings, selling their assets, and taking extra jobs when they should be contemplating retirement, all because they got sick or hurt and couldn’t pay.

That crisis is caused by a confluence of factors.

- Expensive care. The US has the world’s costliest care by a wide margin.

- Inadequate insurance: 50% of insured Americans are on plans with significant out-of-pocket expenses.

- Minimal savings. 56% of Americans can’t cover an unexpected emergency expense[2].

This combination creates a perfect storm of medical debt. Illness and injury are normal parts of life, and they are not predictable. When they are no longer affordable, families are inevitably dragged into debt.

A Broken System

So what happens when patients can’t pay their bills?

- The provider tries to collect. Medical providers across the country spend billions on billing and collection. Some hospitals have more billing clerks than beds.

- The provider fails to collect. The collection rate for expenses not covered by insurance is very low: PayZen estimates it at only 15.5%.

- The account is sold to a collection agency. When providers can’t collect, the account is sold to a debt collector, often for a fraction of the original amount.

- The provider passes the cost on. Providers write off their losses as uncompensated care and pass them on to paying patients. American hospitals provided over $40 billion in uncompensated care in 2020[3].

- The debt collectors pursue the patient. Collection efforts may leave patients with ruined credit. Patients may face harassment, lawsuits and even wage garnishment.

The unpaid amount is effectively collected twice, once by the provider passing the costs on to paying patients and once by the collectors that pursue the patient.

The trend in health care nationally is to put more and more on the patient.

David Cutler, Professor of Applied Economics, Harvard University

This system is a burden for everyone involved except the collection agencies.

- Providers spend enormous amounts on billing and collection and usually fail to collect.

- Insurers face escalated costs. The cost of billing, collection, and uncompensated care is passed on to paying patients, usually those with insurance.

- Insurance premiums rise, an additional cost for employers and employees alike.

- Patients suffer. Patients who can’t pay their bills are continuously in debt, in many cases adding to the mental and financial stress of ongoing illness.

- Costs spiral. Patients who know they can’t pay may avoid needed care, delaying it until their conditions worsen and become far more expensive to treat.

PayZen offers a better approach.

The PayZen Solution

PayZen has developed a healthcare financing solution that addresses the key problems of both providers and patients.

If you select payment through PayZen, they will settle your bill with the provider. They will then negotiate an affordable payment plan with you, using a proprietary AI model to calculate a payment that will not be an exorbitant burden.

PayZen will not charge interest or fees. They will not resort to aggressive collection practices or lawsuits. There’s only a soft pull on your credit record, which will not affect your credit score.

But with no interest or fees, how does PayZen make money?

The answer is simple: they settle your bill for less than what you actually owe. The difference between their settlement and your final payment amount becomes their profit.

PayZen doesn’t reveal, what they pay providers, but they do state that provider collection rates increase by 50%. Providers also get paid upfront with no added billing and collection costs.

The improved collection rate, immediate payment, and lower collection costs make it worthwhile for providers to accept less than the full amount a patient owes.

How it Works

PayZen is a relatively new company and still has limited coverage. At present, PayZen only works through healthcare providers. If your provider is not working with PayZen you cannot use the service, though you can suggest to your provider that they should consider working with PayZen.

PayZen currently works with 30 providers in 15 states in the Gulf, Southeast, Mid-Atlantic, and Midwest regions. The Company is expanding rapidly and expects to have a presence in all 50 states by the end of 2023.

The Company expects to offer services directly to patients in the future but does not have a specific timeline for doing so.

If your provider works with PayZen, there are only three requirements you need to meet.

- You must live in the U.S.

- The care you receive must be necessary (elective cosmetic surgery, for example, would not be eligible).

- Your out-of-pocket cost (after insurance) must be between $250 and $10,000.

Within those restrictions, all patients can be served. There are no credit or income requirements.

If your provider uses PayZen and you meet the three criteria above, you will be approved. Just ask your provider if they work with PayZen. If they do, follow the instructions they give you. If they don’t, suggest that they start!

Key Features

Here are some of PayZen’s most prominent characteristics.

- You pay only what you owe. There’s no interest or fees.

- Payment plans range from three to 60 months.

- Monthly payments are typically between $25 and $100.

- You can request a different due date, monthly payment, or payment term.

- You can request a payment pause if you’re under financial stress.

- Multiple payment methods are available, including checking accounts, debit cards, and HSA/FSA cards. You can change payment methods at any time.

- You can pay early or make larger payments than scheduled at no cost.

- You can remove a bill from your payment plan at any time. The bill will be re-integrated into the provider’s payment system.

- You can cancel your payment plan at any time. The account will be re-integrated into the provider’s payment system.

This array of advantages makes PayZen a clearly advantageous option if you can access their services.

About PayZen

PayZen is a healthcare fintech company based in San Francisco, CA. It was founded in July 2019 by Ariel Rosenthal, Itzik Cohen, and Tobias Mezger.

The Company has raised $240 million in five funding rounds, the most recent in November 2022. Nine venture capital firms have committed money to PayZen, including 7wire Ventures, SignalFire, Viola Ventures, and Picus Capital.

PayZen aims to allow healthcare providers to focus on healthcare rather than financial services and to achieve better financial outcomes for both providers and patients by offering non-recourse patient financing and smart payment plans.

PayZen Competitors

The healthcare payment fintech business is brand new and has attracted a number of participants offering different solutions for patients and providers.

Prima HealthCredit partners with providers to offer financing plans that approve up to 89% of patients. The plans carry interest, and individuals with “challenged credit” will pay rates as high as 24.99%.

Walnut offers financing to patients using participating medical providers. Some credit history is required, and there will be a hard inquiry if you choose a financing plan. There may be interest and fees for financing plans.

Paytient lets employers, insurers, and providers offer an interest-free Paytient Card to cover their out-of-patient costs.

Like PayZen, these services are currently structured as “Buy Now Pay Later” systems offered by participating providers. If your provider is not involved with one of these companies, the services will not be available to you.

Should You Use PayZen?

If you have bills you can’t pay, and your provider offers PayZen as an option, it’s a clearly superior choice, and there’s nothing to lose and much to gain from using it.

The main obstacle right now is the limited number of providers. When choosing a provider, it makes sense to look for one that offers PayZen’s services. They may be difficult to find now, but that will likely change.

The very high level of patient debt and the very low collection rate for uninsured obligations indicate enormous potential demand for these services. We expect rapid adoption by providers and the arrival of systems that allow patients to apply directly rather than through a provider.

Right now, PayZen is available only through a limited number of providers. In a few years, it may be the default choice for dealing with out-of-pocket medical costs.

The post PayZen: A Better Way to Finance Medical Bills appeared first on FinMasters.

FinMasters