Do you understand the many types of interest rates and how they work? You can be sure that lenders, credit card issuers, banks, and other businesses who charge or pay interest know exactly how interest rates work. If you don’t, you’ll be at a disadvantage any time you shop for financial products or negotiate with service providers.

As a consumer, you can do yourself a favor by learning more about how interest rates work for both borrowers and savers. This article will explain how different types of interest rates work in a common language. That should help you build the knowledge you need to make borrowing, saving, and investment choices that work for you.

There are two main types of interest rates that affect you as a consumer: the interest you pay when you borrow money and the interest you earn when you save or invest money.

Interest Rates in Borrowing

When you’re borrowing money, the interest rate is the price a lender charges for your use of their money.

The interest rate a lender charge is based on several factors, such as:

- What is the prime interest rate is

- The borrower’s credit rating

- The loan type

- The lender’s perception of the risk they’re taking

Let’s break these factors down a bit.

1. The Prime Rate

Lenders set their interest rates based on what’s called the Federal Funds Rate. The Federal Reserve sets this rate. This is the rate that banks charge when they lend to other banks.

The prime interest rate or prime rate is the typical interest rate banks charge to the best (least risky) borrowers. In most cases, these are corporate borrowers, and few individuals will qualify. The prime rate is usually around three percent above the fed funds rate. Each bank sets its own rate. The quoted “prime rate” is an average of the prime rates that major banks charge at a given time. As of January 2023, the prime rate is 7.5%.

The prime rate is used as a basis for calculating other types of interest rates, which are often expressed as the prime rate plus a fixed percentage. For example, a variable interest rate may be the prime rate plus 5% or 5% above the prime rate during any given period.

2. The Borrower’s Qualifications

Lenders and credit card issuers base their interests on the perceived risk posed by a borrower. The riskier the transaction, the higher the interest rate will be.

Your credit score is the main tool that borrowers use to evaluate risk, and it has a direct impact on the interest rate you’ll pay. This is true whether you use mortgages, loans, credit cards, or other types of credit. The better your credit score, the better chance you have of paying lower interest rates on the money you borrow.

For example, “subprime” borrowers (credit scores from 501 to 600) paid an average interest rate of 12.93% on car loans in Jan. 2023. Borrowers with “super prime prime” credit scores (781 to 850) paid an average of 3.84%.

Lenders will also consider other factors in their risk assessment, including your education, income, employment history, and debt-to-income ratio.

3. The Loan Type

Lenders charge different interest rates for different types of loans. Secured loans, like a mortgage or car loan, often carry lower rates than unsecured loans, like personal loans or credit cards. That’s because the lender can seize the collateral that secures the loan if you don’t pay. If your loan is unsecured, the lender has fewer options.

Different loans also carry different levels of risk. Most borrowers will prioritize mortgage or car payments over credit card payments, and unsecured loans that can be discharged in bankruptcy carry more risk than secured loans.

For example, the average mortgage interest rate for a 60-month car loan in Jan. 2023 was 4.07%. The average interest rate on a new credit card was 19.07%.

Mortgage Interest Rates

Mortgage interest is a bit different from most other interest rates. A mortgage is one of the only loans that an ordinary borrower with good credit can get at below the prime rate. On Jan. 12, 2023, the prime rate is 7.25% and the average 30 year fixed mortgage rate is 6.25%.

This variance occurs for two reasons:

- Mortgages are long term loans, generally 30 years.

- Mortgages are usually sold in a secondary market, where they compete with bonds for investment buyers.

Because of these factors, mortgage rates tend to be based on bond rates and overall market conditions rather than the short-term prime rate.

Fixed and Variable Interest Rates

Loan companies offer two types of interest rates on loans: fixed rates and variable rates. A fixed interest rate on loan guarantees that you’ll be charged the same interest rate throughout the life of the loan.

If you take on a loan with a variable interest rate, the percentage of interest you’re paying on the loan can (and probably will) fluctuate over time. The interest will usually be the prime rate plus a defined “spread” above that rate.

Many variable interest rate loans offer initial interest rates that you will pay for a fixed period. This rate is usually below the prevailing rate for fixed-rate loans. However, variable rate loans don’t come with the security that fixed rate loans do. When you sign up for a variable rate loan, you’re taking a gamble that the initial lower rate will result in a lifetime of less interest paid. If interest rates go up, the variable interest rate on your loan could go up as well.

Only you can decide if this is a gamble worth taking. Consider the term of the loan: the longer the loan term, the greater the potential for interest rate fluctuations. Also, consider the terms of the variable rate. Most variable rate loans specify the frequency with which your rate can increase, a maximum amount that it can increase at one time, and a maximum rate. All of these factors affect your choice.

Annual Percentage Rates (APR)

When you borrow money or establish a revolving credit line, you may see two figures cited: the interest rate and the Annual Percentage Rate or APR. The APR will be a larger number.

The APR represents the total cost of the credit you are taking on, including the interest and any fees or other costs. If the loan has no costs other than interest, the interest rate and APR will be the same.

You might find two lenders both offering a 5% interest rate on a loan. However, the APR (which must be disclosed on loan papers) for the two loans might be different due to fees and other costs involved with the loan.

It’s important to look at the APR before you sign any loan papers. The APR can give you a more accurate picture of the total cost of the credit you’re applying for.

Interest Rates in Saving and Investing

When you’re saving or investing your money, the interest rate is the money that the bank, bond issuer, or account provider pays you for the use of your money.

If you use someone else’s money, you pay for the use of that money. When someone else uses your money, they pay you for the right to use it.

Interest on Bank Accounts

This occurs when you keep money in a savings account, money market account, certificate of deposit, or other interest-bearing accounts. That money doesn’t just sit in a vault: the bank uses it. They lend it to other people and pay you a portion of their earnings as interest.

Banks charge a higher interest rate for money they lend than the interest rates they pay to deposit account holders. The difference in the two interest rates, called the “spread”, is where the bank earns its profits.

For Example

For Example

Let’s say a bank pays you 1% on your CD balance. At the same time, it charges you 5% for your auto loan, which matches the dollar amount of your CD. They’re making a 4% profit.

Bond Interest

When you invest in bonds, you are lending money to the bond issuer. The bond issuer pays you interest on the money it has borrowed. Like loan interest rates, bond interest rates are higher when the borrower is perceived as a high risk.

For Example

The US government is considered a very low-risk borrower, and the 10-year treasury bond rate (Jan. 12, 2023) is 3.54%. A 10-year bond issued by the Brazilian government carries a 12.43% interest rate, which indicates a higher level of perceived risk.

The same distinction applies to corporate bonds. Rating services evaluate a company’s creditworthiness and assign the company a rating from AAA down to D. That rating is essentially the company’s credit score: highly rated bonds pay lower interest than low-rated “junk” bonds.

Bonds usually pay higher interest than bank accounts because you are lending the money yourself and the interest on the loan goes only to you. When a bank lends the money you have on the deposit, you share the interest paid by the borrower, and the bank generally gets a bigger cut.

Remember that stock market investments and many other investments do not pay interest at all. Actual or expected gains that come from appreciation in asset value are not interest and should not be treated as interest.

Annual Percentage Yield

The term APY (Annual Percentage Yield, sometimes called AER or Annual Effective Rate) is essentially the same concept as APR, except applied to savings and investments. The APY describes the actual yield of an investment or interest-bearing account after any fees are deducted. Just as the APR is usually higher than the cited interest rate, the APY is typically lower than the cited interest rate.

For Example

Investment might offer a return of 5% annually. Including fees, the actual rate of return (APY) might be 4.875%.

It’s important to ask for or look at a contract’s APY before committing to an investment.

Simple Interest

Most installment loans charge what is called simple interest. Your interest payment for a given month is simply calculated from your current loan balance.

The interest rate on a fixed loan stays the same. The balance that the rate is applied to will change as you pay the loan off. Each time you make a payment, your loan balance goes down. Your interest payment each month is calculated on the basis of your current balance, so your monthly interest payment will go down as your balance gets smaller. This process is called amortization.

For Example: If you take out a car loan for $15,000 at a simple 4% interest rate for a two-year loan period, your payment will remain at $651.37 over the life of the loan.

Let’s calculate.

You can (roughly) calculate your interest for that first year by doing some simple math.

$15,000 x .04 / 12 = $50 in interest per month

It’s important to note that you will only pay $50 of interest the first month you have the loan. That interest amount will go down each month because your loan balance will go down each month.

Here’s an amortization schedule on the fictitious two-year loan that can show you what I mean.

| Payment Date | Payment | Principal | Interest | Total Interest | Balance |

|---|---|---|---|---|---|

| Jan 2023 | $651.37 | $601.37 | $50 | $50 | $14,498.63 |

| Mar 2023 | $651.37 | $603.38 | $48 | $98 | $13,795.25 |

| Apr 2023 | $651.37 | $605.39 | $45.98 | $143.98 | $13,189.86 |

| May 2023 | $651.37 | $607.41 | $43.97 | $187.95 | $12,582.45 |

| Jun 2023 | $651.37 | $609.43 | $41.94 | $229.89 | $11,973.02 |

| Jul 2023 | $651.37 | $611.46 | $39.91 | $269.80 | $11,361.55 |

| Aug 2023 | $651.37 | $613.50 | $37.87 | $307.67 | $10,748.05 |

| Sep 2023 | $651.37 | $615.55 | $35.83 | $343.50 | $10,132.51 |

| Oct 2023 | $651.37 | $617.60 | $33.78 | $377.27 | $9,514.91 |

| Nov 2023 | $651.37 | $619.66 | $31.72 | $408.99 | $8,895.25 |

| Dec 2023 | $651.37 | $621.72 | $29.65 | $438.64 | $8,273.53 |

| Jan 2024 | $651.37 | $623.80 | $27.58 | $466.22 | $7,649.73 |

| Feb 2024 | $651.37 | $625.87 | $25.50 | $491.72 | $7,023.86 |

| Mar 2024 | $651.37 | $627.96 | $23.41 | $515.13 | $6,395.89 |

| Apr 2024 | $651.37 | $630.05 | $21.32 | $536.45 | $5,765.84 |

| May 2024 | $651.37 | $632.15 | $19.22 | $555.67 | $5,133.69 |

| Jun 2024 | $651.37 | $634.15 | $17.11 | $572.78 | $4,499.42 |

| Jul 2024 | $651.37 | $636.38 | $15.00 | $587.78 | $3,863.05 |

| Aug 2024 | $651.37 | $638.50 | $12.88 | $600.65 | $3,224.55 |

| Sep 2024 | $651.37 | $640.63 | $10.75 | $611.40 | $2,583.93 |

| Oct 2024 | $651.37 | $642.76 | $8.61 | $620.02 | $1,194.17 |

| Nov 2024 | $651.37 | $644.90 | $6.47 | $626.49 | $1,296.26 |

| Dec 2024 | $651.37 | $647.05 | $4.32 | $630.81 | $649.21 |

| Jan 2025 | $651.37 | $649.21 | $2.16 | $632.97 | $0.00 |

Notice that as payments are made each month, the amount of money going toward reducing the actual (principal) balance of the loan increases. Conversely, the amount of interest you pay decreases.

You can see the financial results of simple interest from the loan amortization table above. Or there’s a formula you can use to figure it out for yourself:

P x I / 365 x N

P x I / 365 x N stands for: the principal balance on the loan times the interest rate, divided by the number of days in a year times the number of days between payments.

So, for the two-year term auto loan example above, you can figure out the first month’s interest by calculating $15,000 x .04 ($600) / 365 (roughly $1.64) x 31 = $50.96.

If it were a 30-day month, the interest you pay during that first month would only be $49.32. And if you made your payments with less or more time between payments, the amount of interest you paid each month would vary as well.

Using calculations like these on simple interest loans or compounding interest investments helps you better determine what you’re actually paying (or earning). You can use our simple interest calculator to help you determine what interest on a given loan or deposit will be.

Compound Interest

Compound interest is interest paid on interest. When an account carries compound interest, the interest amount is added to the balance, and subsequent interest payments are calculated on both the balance and the cumulative interest added.

The interest is added to the balance at regular intervals. Compounding intervals may be daily, weekly, monthly, quarterly, annually, or any other interval fixed by the lender.

To calculate compound interest, you need to know three things:

- The principal amount.

- The interest rate.

- The compounding interval.

The higher the rate and the shorter the compounding interval, the faster the interest will accumulate.

Compound interest can work for you if it’s being paid to you, and it can work against you if you’re paying it.

Earning Compound Interest

Most interest-bearing accounts carry compound interest. That means that you will earn interest on your interest payments as well as the balance. Let’s see how that can work.

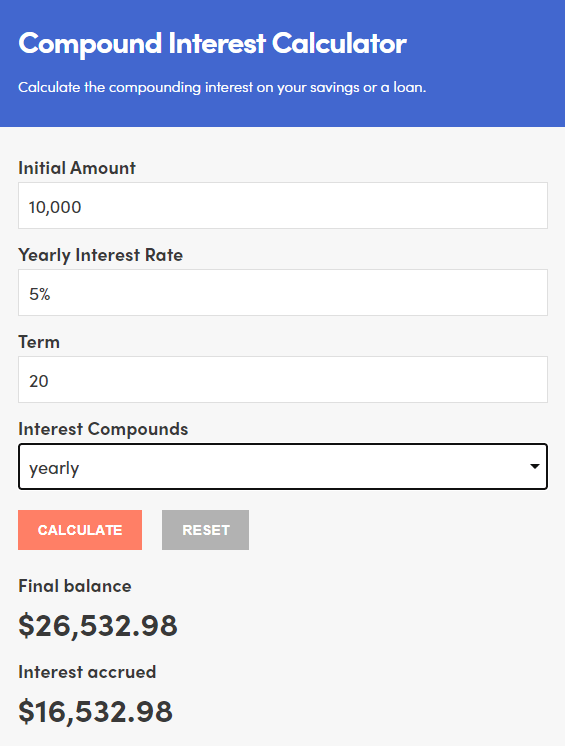

Let’s say you have $10,000 in a fixed investment account earning a 5% return, compounded annually.

At the end of year one, you’ll have an account balance of $10,500. For year two, you’ll now earn 5% on $10,500 instead of simply your initial $10,000. This annual increase in the balance in which you earn interest can help your investment grow over time.

Here’s what I mean.

If you were to not earn compound interest on your $10,000 investment and simply earn your 5% for the next twenty years, you’d have doubled your money by the end of that time.

You’d have $20,000 after 20 years.

However, if you factor in compound interest the amount of money you’d have at the end of 20 years changes dramatically. Let’s run those numbers through the FinMasters compound interest calculator and see what we get.

As you can see, compound interest gains you an additional $6,532.98.

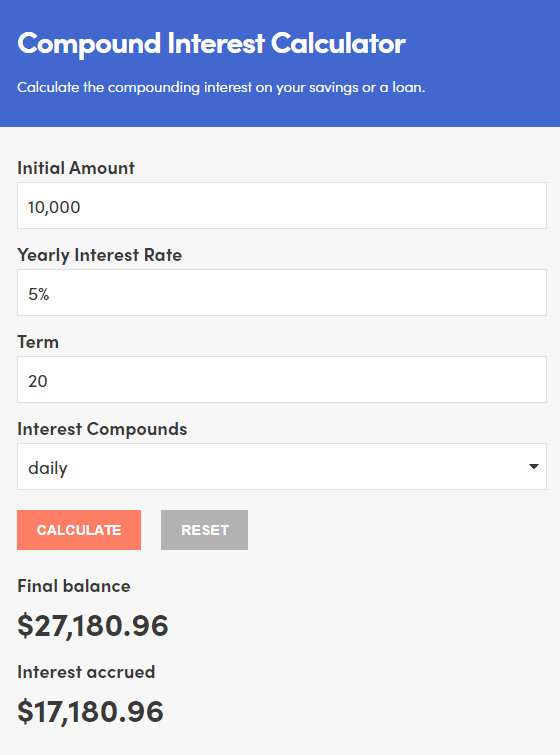

Now let’s look at what happens if the interest is compounded daily.

The change in compounding interval earns you almost $650 extra.

The higher the rate and the more frequent the compounding interval, the faster compound interest will accumulate…

Paying Compound Interest, or Why Credit Card Debt is So Dangerous

Compound interest can work for you if you’re earning it, but it can work against you if you’re paying it. This happens most frequently with credit card debt. Credit card debt presents unique risks, which come from the collision of four factors.

- Low minimum payments. Many cards allow you to keep your account in good standing with a relatively accessible minimum monthly payment.

- Revolving credit. Credit cards allow you to keep spending. You can add to your balance faster than you pay it off, and many users do.

- High interest rates. The average US card rate is 14.65%, and if your credit isn’t great you may be paying well over 20%

- Compound interest. Credit cards carry compound interest and the interest is usually compounded daily.

What does that mean in practice?

For Example

Let’s say you have a $5000 balance on a card with a 15% interest rate and a minimum payment of 2%.

If you make only the minimum payment each month, it will take you 27 years and six months to pay off that balance, and you will pay a total of $12,517.52… and that’s assuming you make no additional purchases with the card.

Many credit card users have been caught in that trap, and knowing more about how to pay off credit card debt can help you avoid being one of them.

Some financial analysts describe earning compound interest as “magic”. If that’s the case, paying compound interest – especially with a high rate and daily compounding – might be called black magic.

Summary

Knowing at least a little bit about the different types of interest rates is important. This is true both for investors and borrowers. At the bare minimum, you should understand the following terms:

- Prime interest rate – The rate offered to the best (least risky) borrowers.

- Compound interest – Interest that incorporates previous interest payments into the calculations.

- Simple interest – Interest that is wholly based on the original sum invested or loaned.

- Annual percentage rate – The interest rate on a loan when fees are included.

- Annual percentage yield – The interest rate on a savings account or other investment after accounting for fees.

- Fixed interest – An interest rate that stays the same for the duration of a loan.

- Variable interest – An interest rate that can (and probably will) fluctuate during the time it takes to pay off a loan.

Knowing these different types of interest rates will make financial planning easier, whether you’re taking on debt, paying off debt, saving, or investing.

The post Types Of Interest Rates in Borrowing, Saving & Investing appeared first on FinMasters.

FinMasters