A credit score is a numerical representation of the risk of you defaulting on a loan. It ranges from 300 to 850. The higher the number, the less likely you are to default.

Credit scores are provided by two companies: FICO® and VantageScore. These companies base their scores on information in your credit reports from the three major credit bureaus: Experian, Equifax and TransUnion. They run this information through proprietary algorithms to produce your score.

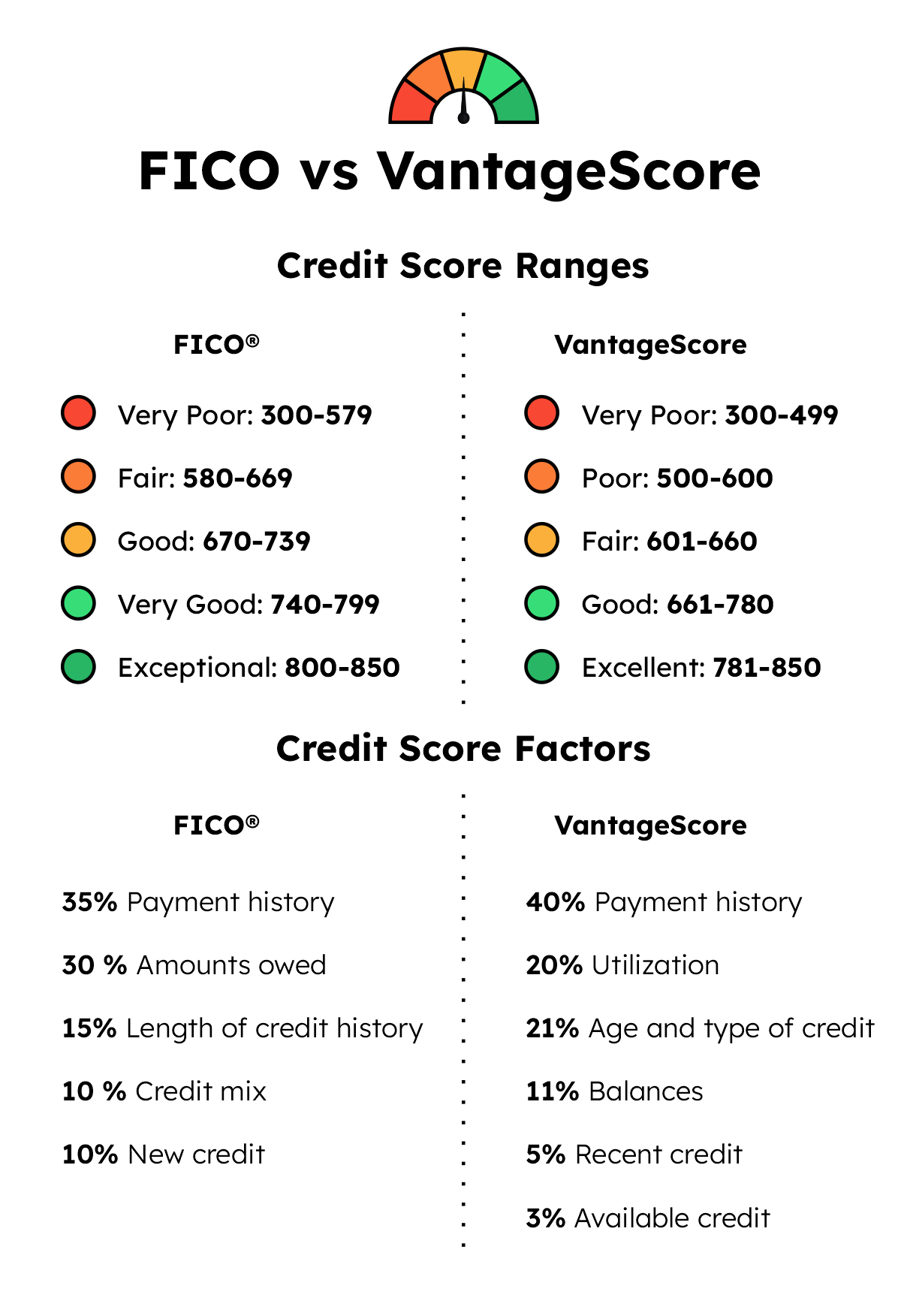

Let’s take a look at what constitute a good FICO score as well as what a good VantageScore might be.

What Is A Good FICO Score?

“FICO” stands for Fair Isaac Corp., the first company to develop a widely used numerical credit rating scheme.

FICO classifies any score between 670 and 739 as “good”. Scores between 580 and 669 are regarded as “fair,” while 740 and 799 are regarded as very good. Anything above 800 is considered “exceptional.”

What Is A Good Rating With VantageScore?

FICO competitor VantageScore generates a similar rating using the same credit reports. The VantageScore algorithm is different, so the scores will not be the same as FICO scores.

VantageScore classifies scores from 661 to 780 as “good”. VantageScores 780 to 850 are considered “exceptional”, whereas those between 601 and 660 are “fair.” VantageScores lower than 600 are considered “poor.”

How Many Americans Have a Good Credit Score?

The average American Fico score in April 2022 was 716, which is squarely in the “good” range. Here’s how the scores break down:

67% of Americans with credit scores have good, very good, or excellent credit. Only 33% have fair or poor credit. Those percentages don’t include the 45 million adults who have no credit score!

What Will a Good Credit Score Get Me?

The score ranges we discussed above are set by FICO and VantageScore. Individual lenders may use different ranges. For example, lenders making secured loans, like mortgages and car loans, may accept lower scores because the loan is protected by collateral.

A score that is “good” to FICO or VantageScore may not be in the same category for any given lender. Still, as a general rule, you can expect to get approved for most loans and credit cards with a “good” score, especially if you’re in the upper part of the “good” range.

While you will get approved, you may not get the lowest rates ot the best terms, which are reserved for borrowers in the “very good” and “excellent” ranges. You may not be approved for premium products, like the credit cards with the highest rewards.

If you aim for perfection, you should know that only 1.3% of borrowers have a perfect credit score. Fortunately, it doesn’t matter much[1]. An 800 score will get you the same deals as an 850 credit score.

Once you’re in the “excellent” range, lenders and card issuers will roll out the red carpet!

Most lenders will be very happy with an 800 credit score, but the size of the loan they will offer will not just depend on your credit score.

The size of the loan you’re offered will also depend on your income, assets, and debt-to-income ratio. Lenders making secured loans will lend more than lenders making unsecured loans.

Your 800 score makes it easier to get a loan but does not determine the size of that loan.

A 700 credit score is in the “good” range but below the US average. You will qualify for loans and credit cards, but you won’t get the best interest rates or terms, and you may not qualify for premium products.

If you’re considering a major loan, like a mortgage or car loan, it’s worth working on your credit score first. Even a modest increase could save you thousands of dollars over the life of the loan.

You can get loans and credit cards with a 650 credit score, but don’t expect the best interest rates, and be prepared to document a good income and an acceptable debt-to-income ratio.

You will have to shop for lenders who will consider a 650 score because not all do. Do some research on minimum credit scores before you apply. You don’t want to apply for loans you aren’t going to get!

Credit Scoring Factors

A number of factors are used to calculate your credit score. Although the exact criteria used by each rating model vary, the following are the most important influences on your FICO score.

- Payment History: on-time payments are the single most important part of your credit score.

- Credit Utilization: credit utilization is the percentage of your credit limit that you are using on your revolving accounts, like credit cards.

- Length of Credit History: based on the average age of your active credit accounts.

- New Credit: each time you apply for credit, a hard inquiry is placed on your account.

- Credit Mix: your credit mix is the balance between installment credit and revolving credit.

VantageScore uses very similar criteria, though they are weighted differently.

Understanding how your credit score is calculated is an important step toward improving it.

Tip: Tax liens, civil judgments, alimony, and child support obligations do not appear in credit reports. However, lenders can locate them through public records, and they will affect your ability to get credit.

Tip: Tax liens, civil judgments, alimony, and child support obligations do not appear in credit reports. However, lenders can locate them through public records, and they will affect your ability to get credit.

The Benefits of a Good Credit Score

Your credit score is designed to measure the risk that you will default on your loan obligations. It’s used for many purposes outside of lending, though. Here are some of the benefits of a good credit score:

- Easier qualification. Whenever you apply for a loan, credit card, or any other type of credit, the lender will verify your credit score. Good scores make it easier to qualify.

- Better interest rates. Lenders offer lower rates to low-risk borrowers. The savings can be significant.

- Better access to employment. Some employers will verify your credit score before making a hiring decision.

- Renting gets easier. Landlords will check your credit before renting you a house or apartment.

- Avoid Expensive Types of Credit. If you can’t get approved for loans or credit cards, you might have to use costly forms of credit, such as payday loans, to cover a deficit.

Think of your credit score as a financial report card. A passing grade makes your entire financial life easier!

How To Improve Your Credit Score

You can improve your credit score. Here are some ways to start:

- Get a free copy of your credit report. Understanding what’s on your credit report can help you learn what is helping or hurting your score.

- Dispute inaccurate information on your report. Your scores may suffer due to incorrect information in your credit file. If you see inaccurate information on your credit report, dispute it at once.

- Make any outstanding payments. Late payments and delinquent accounts are credit score kryptonite. Get your payments current and keep them that way!

- Set Up More Frequent Payments. Making payments several times a month will help you keep your balance down and lower your credit utilization ratio.

There are many other ways to build credit, but the most effective are the most basic: make your payments on time and keep your credit card balances low!

Tip: Do not close any credit cards you have paid off. Closing accounts raises your credit utilization ratio and shortens the average age of your credit accounts.

FAQ

Paying bills on time is the single biggest contributor to a good score. Being behind on any payment for any length of time will hurt your score badly.

You have many credit scores. Your credit scores may be different if the information is sourced from different credit bureaus. Credit score providers also provide specialized credit scores for specific uses, like auto loans and credit cards.

All of these scores are based on information in your credit reports, but the information may be processed differently or sourced from different credit bureaus.

Credit scores are calculated by credit scoring companies, mainly FICO and VantageScore. They are based on information in credit reports collected by the three major credit bureaus: Experian, Equifax, and TransUnion.

Contrary to popular belief, your score does not begin at 300. You start out with no score at all: if you have no credit record or very few records, you will not be considered scorable. If you make regular payments on several loans or credit cards, you will accumulate a respectable score of approximately 700 easily within a few months.

Most medical organizations do not report to credit bureaus. However, if an account is sold to a collection agency or you use credit cards to pay medical bills, you can hurt your credit score.

The answer used to be “no”, but two services can now help you include bill payments for credit bureaus. Sign up with Experian BOOST or eCredable Lift. This can improve your score by up to 15 points. Not all scoring models will include this information.

or eCredable Lift. This can improve your score by up to 15 points. Not all scoring models will include this information.

The post What Is A Good Credit Score and Why It Matters appeared first on FinMasters.

FinMasters